Small Business Accounting Basics

Small Business Accounting Basics – Let’s be honest, the words “small business accounting” don’t exactly set the world on fire. For many entrepreneurs, it feels like a chore—something you have to do, not something you want to do. But what if I told you that mastering the basics isn’t about bookkeeping? It’s about building a navigation system for your company.

Think of it as the map and compass that guide you from a hopeful startup to a thriving, successful business. It helps you make smarter decisions, gives you the confidence to talk to banks, and makes tax season a breeze.

Why Accounting Basics Are Your Business Compass

Starting a business without a grip on your finances is like setting sail without a map. You might have a brilliant idea and a clear destination in mind, but you’re essentially navigating blind, hoping you don’t run into any hidden rocks or get caught in a storm.

This is where understanding basic accounting becomes your secret weapon. It’s not just about ticking boxes for HMRC; it’s the skill that turns you from a passenger on your own ship into a confident captain, steering your business exactly where you want it to go.

With clear financial insights, you can chart a reliable course for growth. You’ll see the flow of money in and out of your business, helping you dodge the financial icebergs that sink so many new ventures. It’s about being proactive, not just reacting when a crisis hits.

Charting Your Course with Financial Data

Your financial records are your ship’s logbook. Every sale, every expense, every invoice tells a part of your story, revealing what’s working and what isn’t. Good accounting organises all that data into a clear narrative, helping you answer the really important questions:

- Are we actually making money? It’s easy to confuse revenue with profit. For example, a catering business might have £10,000 in sales, but after factoring in food costs, staff wages, and van fuel, is the profit £2,000 or just £200? Your accounts tell you the real story.

- Can we pay the bills next month? Cash flow is king. You might have sent invoices for £5,000, but if only £1,000 has been paid and you have a £3,000 payroll due, you have a problem. Your records will highlight this potential shortfall.

- Is it time to grow? Can you really afford to invest in that new piece of equipment or hire another team member? Your numbers will tell you if the cash is there and if the projected return on investment makes sense.

This kind of clarity is absolutely vital in the UK’s competitive market. The number of small businesses has shot up by 26.4% over the past decade, even with all the economic headwinds. This just goes to show how resilient UK entrepreneurs are, but it also means sharp financial management is essential to stand out. You can dive deeper into these trends over at money.co.uk.

Accurate accounting provides the ultimate competitive edge. It replaces guesswork with certainty, allowing you to steer your business towards sustainable success with precision and confidence.

Beyond Day-to-Day Operations

Ultimately, solid accounting fundamentals do more than just keep your books tidy. They build trust with banks and investors, making it far easier to secure funding when you need it.

They also transform tax season from a frantic, stressful scramble into a predictable, manageable process. You’ll know what you owe HMRC, with no costly surprises. By getting to grips with these basics, you’re not just managing money; you’re building a resilient, successful, and future-proof business.

Understanding the Core Pillars of Accounting

To get a real grip on your business finances, you first need to learn the language they speak. Let’s pull back the curtain on a few core concepts that form the bedrock of all small business accounting. These aren’t just buzzwords; they’re the rules of the game that dictate how your financial story gets told.

Think of these pillars as the grammar of your business’s financial language. Once you get the hang of them, reading your financial reports will feel like second nature.

The Fundamental Accounting Equation

Right at the heart of bookkeeping is a beautifully simple formula: the accounting equation. It’s the one non-negotiable rule that ensures your books are always balanced, no matter what.

Assets = Liabilities + Equity

Let’s break this down with a practical example. Imagine you’ve just launched a small bakery.

- Assets: These are all the valuable things your business owns. It’s the £2,000 cash in your business bank account, that expensive new £8,000 oven you bought, and the £500 a corporate client owes you for a large cake order (known as ‘accounts receivable’).

- Liabilities: This is everything your business owes to other people. It could be the £6,000 bank loan you took out for that oven, the £300 bill you haven’t yet paid your flour supplier, or your £200 business credit card debt.

- Equity: This is what’s left over after you subtract what you owe (liabilities) from what you own (assets). It’s your stake in the business—the portion that is truly yours.

Let’s see the equation in action. Your bakery buys a new delivery van for £15,000. You pay £5,000 in cash from your business bank account (an asset) and take out a £10,000 loan (a liability) to cover the rest.

Here’s how the equation stays perfectly balanced: Your assets go up by £15,000 (the new van) but also go down by £5,000 (the cash you spent), giving you a net asset increase of £10,000. At the same time, your liabilities have increased by £10,000 (the new loan). The equation holds true.

Choosing Your Accounting Method

Next up, you have to decide how you’re going to record your transactions. There are two main methods, and your choice determines when income and expenses officially hit your books.

- Cash Basis Accounting: This is the straightforward one. You record income only when the cash actually lands in your bank account, and you record an expense only when you physically pay for it. Simple.

- Accrual Basis Accounting: This method is a bit more sophisticated. It records income when you’ve earned it and expenses when you’ve incurred them, regardless of when the money actually moves. This gives you a much more accurate picture of your business’s health over a period of time.

Let’s say a freelance graphic designer finishes a project and sends an invoice for £1,000 on the 25th of March. The client doesn’t pay up until the 10th of April.

Under the cash method, that £1,000 income is recorded in April. But under the accrual method, the income gets recorded in March—the month the work was actually done and the money was earned.

To make this clearer, let’s look at a side-by-side comparison for a small consultancy that has just completed a project.

Cash vs Accrual Accounting: A Practical Comparison

| Scenario | Cash Basis Accounting | Accrual Basis Accounting |

|---|---|---|

| 20th Feb: A consultant completes a project and issues a £2,500 invoice. | No entry is made yet. The money hasn’t been received, so there’s no income to record. | Income of £2,500 is recorded immediately. The work is done and the money is earned. |

| 5th Mar: The client pays the £2,500 invoice in full. | The £2,500 income is now recorded. The cash has arrived in the bank. | No income entry is needed. It was already recorded back in February when it was earned. |

| 31st Mar: The consultant reviews their Q1 (Jan-Mar) performance. | The Q1 report shows £2,500 of income, recognised in March. | The Q1 report shows £2,500 of income, recognised in February. |

As you can see, the accrual method gives a truer picture of when the business activity actually happened, which is crucial for making informed decisions.

Organising with a Chart of Accounts

Finally, you need a system to keep all of these transactions organised. That’s where the Chart of Accounts comes in. Don’t let the formal name put you off; it’s basically just your financial filing cabinet.

Think of it like setting up folders on your computer. You’d create main folders (Assets, Liabilities, Equity, Income, Expenses) and then create subfolders inside each one.

For example, inside your main “Expenses” category, a marketing agency might have sub-accounts like “Software Subscriptions,” “Advertising Costs,” “Client Entertainment,” and “Office Supplies.” A plumbing business, on the other hand, would have sub-accounts like “Van Fuel,” “Tools & Equipment,” and “Materials.” This simple structure makes it incredibly easy to see exactly where your money is coming from and where it’s going.

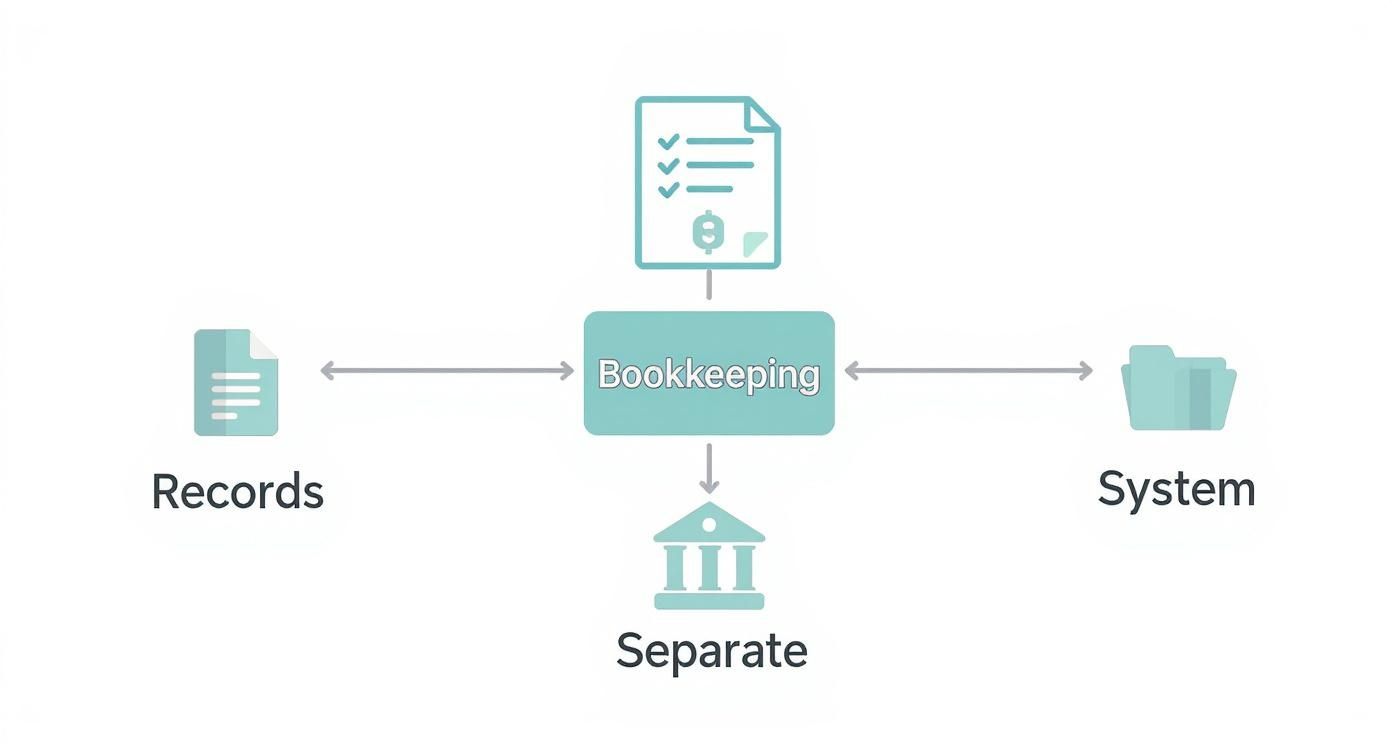

Streamlining Your Bookkeeping and Record Keeping

Good accounting starts with good records. Let’s be clear: effective bookkeeping isn’t about mastering complex formulas. It’s about building a simple, reliable habit of tracking the money flowing in and out of your business. Get this right, and you’ll have a clear view of your financial health.

The aim is to turn that messy pile of receipts and invoices into a clear story of your business’s performance. Whether you use a tidy digital folder system or an old-school filing cabinet, consistency is the key. Nailing this from day one will save you countless hours and headaches down the line, especially when HMRC comes calling.

The Golden Rule: Separate Your Finances

Before you even think about recording a transaction, there’s one non-negotiable rule you must follow: separate your business and personal finances. This isn’t just a tip; it’s the single most important step you can take for financial clarity and legal protection.

Mixing your funds is like trying to bake a cake in a bowl that’s still full of last night’s spaghetti bolognese—the result is a confusing, unusable mess. When your morning coffee and a supplier payment come out of the same account, it becomes almost impossible to figure out if your business is actually profitable.

The solution is refreshingly simple:

- Open a dedicated business bank account. This is your first and most crucial move. All your business income should go into this account, and every business expense should come out of it.

- Get a separate business credit or debit card. Use this card exclusively for business purchases, from software subscriptions to client lunches.

This separation isn’t just a good habit; it’s a professional necessity. It protects your personal assets if the business runs into trouble and makes your financial records clean and credible for lenders, investors, and the tax man.

What Records Do You Need to Keep?

Knowing which documents to hang on to is essential for keeping HMRC happy and for backing up the numbers in your accounts. Your record-keeping system, whatever it looks like, should be designed to store these key items securely.

The core principle of good bookkeeping is simple: for every number in your accounts, there should be a source document to prove it. This creates an audit trail that builds trust and ensures accuracy.

A Practical Example: A Simple Sale

Let’s say your graphic design business completes a project for a client and they pay you £500. Here’s the process:

- Create and Send an Invoice: You issue invoice #001 for £500. Keep a digital copy.

- Record the Payment: When the client pays, the £500 lands in your business bank account.

- File the Documents: You save a copy of the invoice and match it to the bank statement transaction showing the payment.

Another Example: An Everyday Expense

Now, imagine you buy a new office chair for £120 using your business debit card.

- Keep the Receipt: Whether it’s a paper receipt or an email confirmation, this is your proof of purchase.

- Categorise the Expense: You’ll log this under an “Office Furniture” or “Equipment” category in your books.

- Match to Bank Statement: The £120 transaction on your business bank statement confirms the payment.

This simple process, repeated for every single transaction, is the beating heart of effective bookkeeping. It transforms chaotic paperwork into a powerful tool for understanding your business.

With small and medium-sized enterprises (SMEs) making up over 99% of all UK businesses, establishing these foundational habits is what separates the thriving from the struggling. It’s estimated there will be around 5.5 million SMEs by 2025, making organised operations more vital than ever. You can find out more about the UK’s small business landscape on airwallex.com.

How to Read Your Key Financial Statements

Think of financial statements as the storybooks of your business. They take all your hard work—every sale, every purchase, every payment—and translate it into a clear narrative about your company’s performance and financial health. Learning to read them is one of the most powerful skills you can develop as a business owner.

Let’s demystify the ‘big three’ reports that form the core of any good accounting setup. To make it real, we’ll use a local coffee shop as our running example and see how these statements work together to tell a complete financial story.

The Profit and Loss Statement: Your Business Report Card

First up is the Profit & Loss (P&L) Statement, which you might also hear called an Income Statement. This is your business’s performance review over a set period, like a month or a quarter. It answers one simple but crucial question: “Are we profitable?”

It gets to the answer by subtracting all your costs and expenses from your total revenue.

Imagine our coffee shop generated £8,000 in sales last month. The cost of the actual coffee beans, milk, and cups came to £2,500. On top of that, staff wages, rent, and utilities totalled £4,000. The P&L would lay this all out to show a net profit of £1,500 for the month (£8,000 – £2,500 – £4,000). It’s a straight-up measure of your operational success.

The Balance Sheet: A Financial Snapshot

While the P&L looks at performance over time, the Balance Sheet is a snapshot of your business’s financial health on a single day. It clearly lists what your business owns (Assets) and what it owes (Liabilities), all while sticking to that fundamental accounting equation we talked about earlier.

Assets = Liabilities + Equity

For our coffee shop, its assets might include £5,000 cash in the bank, a £10,000 espresso machine, and £1,000 of coffee beans in the stockroom. Its liabilities could be a £6,000 loan for that fancy machine and £500 owed to a supplier. The final piece, the equity—what’s left for the owner—would be £9,500. This report instantly shows you the company’s net worth at that specific moment.

The infographic below really drives home how core bookkeeping concepts—like keeping good records and separating your finances—are the bedrock for creating these reports accurately.

It’s a great visual reminder that a strong, consistent bookkeeping system is what gives you financial statements you can actually trust.

The Cash Flow Statement: Your Liquidity Tracker

Finally, we have the Cash Flow Statement. For day-to-day survival, this might be the most critical report of all, as it tracks the actual, physical cash moving in and out of your business. A key lesson for any owner is that profit on the P&L doesn’t always equal cash in the bank.

This statement breaks down all cash movements into three areas:

- Operating Activities: Cash that comes from your main business activities (like all those flat whites and croissants you sold).

- Investing Activities: Cash spent on or received from selling long-term assets (like buying a new display fridge).

- Financing Activities: Cash from investors or loans, or cash used to repay debt.

Our coffee shop might look profitable on its P&L, but if it just spent £3,000 on a new oven (an investing activity), its cash balance could be dangerously low. This statement is what flags that kind of risk, helping you manage your liquidity before it becomes a problem. Understanding this is so important, and you can learn more about managing your money effectively in our guide on how to improve cash flow. At the end of the day, this report helps ensure you always have enough cash on hand to pay your bills and your team.

Navigating UK Tax and Compliance with Confidence

Staying on the right side of His Majesty’s Revenue and Customs (HMRC) isn’t just a good idea; it’s a non-negotiable part of running a business in the UK. If you manage your tax obligations proactively, you’ll avoid costly penalties and gain some much-needed peace of mind. Think of it less as a chore and more as a core business function.

This part of your financial journey is all about understanding the key taxes that apply to your business and the systems you need to manage them. Let’s create a clear roadmap for your UK tax and compliance duties, turning them from a source of stress into just another manageable task on your to-do list.

Key UK Business Taxes Explained

For most small businesses, there are only a handful of key taxes you need to get your head around. Knowing which ones apply to you is the first, and most important, step towards full compliance.

- Corporation Tax: If you operate as a limited company, you must pay Corporation Tax on your profits. For example, if your company made a profit of £60,000, you would calculate and pay Corporation Tax on this amount.

- VAT (Value Added Tax): This is a tax on most goods and services. You must register for VAT if your VAT-taxable turnover goes over £90,000 in any 12-month period. For instance, if you’re a web designer billing £8,000 per month, you will cross this threshold and need to register.

- PAYE (Pay As You Earn): If you employ staff (and that includes yourself as a director of a limited company), you must register as an employer. This means operating the PAYE system, where you deduct Income Tax and National Insurance from wages before paying them to HMRC.

Think of tax compliance as the scheduled maintenance for your business engine. Neglecting it can lead to a breakdown, but staying on top of it ensures everything runs smoothly and efficiently, helping you avoid unexpected and expensive repairs down the road.

Understanding Allowable Business Expenses

One of the most powerful tools in small business accounting is legally reducing your tax bill through allowable business expenses. These are simply the costs you incur “wholly and exclusively” for business purposes. When you claim them correctly, you lower your taxable profit, which means you pay less tax. It’s as simple as that.

Practical Example: A Landscaper

A self-employed landscaper buys a new lawnmower for £400 and spends £50 on fuel for their van to travel between jobs. Both the lawnmower and the fuel are allowable expenses because they are absolutely essential for running the business.

Practical Example: A Freelance Consultant

A consultant working from home pays for a £30 monthly subscription to a specialist industry journal. They also travel by train to meet a client, which costs £45. Both the subscription and the travel are directly related to their work and can be claimed as expenses.

To get a better idea of what you can claim, check out our comprehensive guide covering sole trader tax deductions for more examples.

Making Tax Digital and Deadlines

The UK is steadily moving towards a fully digital tax system with its Making Tax Digital (MTD) initiative. If your business is VAT-registered, submitting returns through MTD-compatible software is already mandatory. The whole point is to make tax admin more effective, more efficient, and less prone to errors.

Finally, always be aware of your deadlines. This can’t be stressed enough. Missing a submission date for your tax return or a payment deadline will trigger automatic penalties from HMRC. Mark those key dates in your calendar for Self Assessment, Corporation Tax, and VAT returns to make sure you file and pay on time, every time.

Choosing Your First Accounting Tools

Picking the right accounting tool can turn financial management from a chore you dread into a simple, confidence-boosting routine. But what’s “right” depends entirely on where your business is today. What works for a freelance sole trader is worlds away from what a growing limited company with a payroll needs.

For many new entrepreneurs, a well-organised spreadsheet is a perfectly sensible starting point. It costs nothing and gives you a hands-on feel for your income and outgoings. But as your business grows, so does the number of transactions. Manual entry soon becomes a time-sink, and the risk of a typo throwing your numbers off balance gets higher and higher.

That’s the point where dedicated accounting software becomes a real game-changer.

From Spreadsheets to Software

Making the jump from a spreadsheet to proper software is a key milestone in professionalising how you handle your finances. Modern cloud-based platforms like Xero, QuickBooks, and FreeAgent are built from the ground up for small businesses, offering powerful features that spreadsheets just can’t compete with.

These tools do much more than just log numbers; they streamline your whole financial world. They can automate invoicing, let you snap and track expenses with your phone, and link directly to your business bank account to pull in transactions automatically. All this automation frees you up to focus on what you’re best at—running your business.

Let’s be realistic, the financial climate for UK businesses is tough. In fact, 85% of SMEs have reported a major spike in their running costs. When margins are that tight, having efficient tools to manage your cash flow isn’t a luxury; it’s critical for survival.

A Practical Checklist For Your Decision

The number of software options out there can feel overwhelming, but breaking it down makes the choice much simpler. Use this checklist as a guide to compare your options and find the perfect fit.

- Cost: Does the software have a subscription that fits your budget? For example, plans often start around £10-£15 per month for basic features, scaling up to £30+ for payroll and multi-currency options.

- Scalability: Can this tool grow alongside you? Make sure it can handle more complex needs later on, like payroll, stock management, or multi-currency transactions.

- Key Features: Does it have the essentials you need right now? Think professional invoicing, expense tracking, bank reconciliation, and generating key financial reports.

- MTD Compliance: Is the software HMRC-approved for Making Tax Digital? This is non-negotiable for VAT-registered businesses and is set to become essential for almost everyone else.

Think of the right accounting tool not as an expense, but as an investment in efficiency, accuracy, and clarity. It gives you the real-time financial data you need to make smarter, faster business decisions.

Ultimately, the best tool is the one that gives you a clear, up-to-the-minute view of your financial health. It helps you manage your money effectively—a skill you can sharpen with our free cashflow forecast template. By choosing wisely now, you’re building a solid foundation for sustainable growth.

Your Top Small Business Accounting Questions, Answered

When you’re getting to grips with your business finances, a few questions always seem to pop up. Think of this as a quick-fire round to clear up those common uncertainties, giving you the confidence to build your business on a solid financial footing.

Do I Really Need an Accountant for My Small Business?

It’s a fair question. When you’re just starting, you can absolutely manage your own books. But it’s best to see a good accountant as an investment in your future, not just another cost. They do so much more than just file your taxes at the end of the year.

A great accountant acts as a financial guide. They can spot allowable expenses you might have missed—often saving you more in tax than their fee costs. As you grow, their strategic advice on cash flow, profitability, and compliance becomes invaluable. They handle the complex stuff, freeing you up to do what you do best: run your business.

How Often Should I Do My Bookkeeping?

The one-word answer? Consistently. The longer answer is that you should aim to update your records at least once a week.

Sticking to this simple habit stops that dreaded mountain of receipts and invoices from piling up, which can cause a huge headache at year-end. More importantly, it gives you a real-time, accurate picture of your business’s health. This means every decision you make—whether to buy new equipment or take on a new client—is based on up-to-date facts, not guesswork. Modern accounting software can even link to your bank, making this a quick five-minute job.

What Is the Biggest Accounting Mistake to Avoid?

By far, the most damaging mistake small business owners make is mixing their business and personal finances. It seems harmless at first, but it quickly creates a bookkeeping nightmare, makes it impossible to see how your business is really performing, and can land you in hot water with HMRC.

From the very first day, open a separate business bank account. It is the single most important and effective step you can take. This simple action brings instant clarity and creates a vital legal separation between your personal assets and your business liabilities.

Ready to build a stronger financial foundation for your business? At Grow My Acorn, we provide the practical information and advice entrepreneurs need to succeed. Explore our resources and take control of your finances today.

More Topics

What is invoice factoring: A Clear Guide to Faster Cash Flow

Discover what is invoice factoring and how it unlocks fast cash flow for your business with simple examples and practical steps.

12 Profitable Self Employment Ideas to Start in 2025

Discover 12 practical self employment ideas you can launch this year. Our guide covers startup costs, skills, and

How to Delegate Effectively: Master Your Team Productivity

Discover how to delegate effectively with practical tips to boost team productivity, empower others, and drive better results.

How to Build an Email List from Scrath

Learn how to build an email list with our practical guide. Discover actionable strategies and expert tips to grow an audience that converts.

How to Improve Employee Retention

Discover how to improve employee retention with actionable strategies on leadership, compensation, and culture

Streamlining business processes: Boost efficiency today

Discover how streamlining business processes can unlock efficiency and drive growth with practical, actionable steps.

marketing tips for small business: 5 quick wins

Uncover marketing tips for small business that boost ROI with 5 practical strategies you can implement this week

what is professional indemnity insurance? A quick guide

what is professional indemnity insurance: learn what it covers, who needs it, and how to choose the right PI policy for your business.

10 Actionable Marketing Tips for Small Businesses in 2025

Discover 10 practical marketing tips for small businesses. Boost your growth with budget-friendly strategies for SEO,

10 Profitable Business Ideas UK from Home for 2025

Discover 10 practical profitable business ideas UK from home. This guide covers startup costs, income potential,

What Is a Break Even Analysis Explained

What is a break even analysis? Learn how to calculate it and use this simple tool to make smarter financial decisions for your business.

How to Create a Cash Flow Forecast That Works

Learn how to create a cash flow forecast with this practical guide. We cover predicting inflows, mapping outflows,

How to Write a Business Proposal That Wins Clients

Learn how to write a business proposal that actually wins clients. Offering advice and real-world examples

What Is Equity Dilution for Founders

Understand what is equity dilution and how it impacts your startup. Our guide explains cap tables, funding rounds

How to Conduct Competitor Analysis That Drives Growth

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

How to Register a Business in the UK Your Complete Guide

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

12 Best Ways to Advertise Your Business in 2025

12 Best Ways to Advertise Your Business Discover the best ways to advertise your business

Business Exit Strategy Planning Done Right

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Find Business Partners That Actually Fit

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

High Street vs Digital Business Banking

Compare High Street vs Digital Business Banking for start-ups. Discover the pros and cons of business banking

10 Crucial Pieces of Business Advice for Startups

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

How to Scale a Business The Right Way

Learn how to scale a business with proven, real-world strategies. The complete guide

A Board Meeting Agenda Template That Actually Works

Tired of unproductive meetings? Use our board meeting agenda template to drive focus, ensure compliance

Sole Trader Tax Deductions

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Build Business Credit for Your UK Business

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

What Is a Business Model Canvas?

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Improve Customer Service A UK Business Guide

Discover how to improve customer service with actionable strategies for UK businesses

Dealing with Difficult Clients: Top Strategies for Success

Dealing with difficult clients isn’t about winning arguments. Learn how to deal with difficult clients.

Business Plan Executive Summary Examples: 8 Inspiring Samples

How to professionally prepare your business plan executive summary along with practical examples.

Your Guide to a Business Risk Management Framework

Build a robust business risk management framework with our free online guidance.

How to Improve Cash Flow: Proven Tips for UK Businesses

Learn how to improve cash flow with actionable strategies for UK businesses. Master invoicing, managing expenses

Social Media Marketing for Small Business

Social Media Marketing for Small Business Free Expert Guidance from Grow My Acorn the ultimate free resource

10 Powerful Customer Retention Strategies for 2025

Discover 10 actionable customer retention strategies with real examples. Learn how to boost loyalty,

How to Grow a Business The Right Way

How to Grow a Business The Right Way grow your business the right way with free expert advice

Proven Marketing Strategies for Small Businesses

Get your marketing strategy off to a flying start with our proven strategies guaranteed to deliver measurable results.

Sole Trader vs Limited Company UK Guide

Choose the right business structure. Understand the differences, benefits and pitfalls. Sole Trader? Limited Company?

How to Start a Business in the UK

How to start a business in the UK – Your handy free expert guide on how to start a business in the UK

How to Protect Your Business with Contracts and Agreements

Learn how to protect your business with contracts and agreements. A practical guide for startups

Taking the Leap: The Ultimate Guide to Hiring Your First Employee

Thinking of hiring your first employee? Take a look at our handy guide to understand when and how to recruit.

10 Proven Low-Cost Marketing Strategies for Startups

10 proven low costs marketing strategies which you can implement today to grow your business.

How Much Does It Really Cost to Start a Small Business

Wondering how much it costs to start a small business in the UK? Discover the real start up expenses for entrepreneurs,

Top 20 Home Based Business Ideas

Looking for the best home based business ideas? Discover 20 profitable ways to start a business from home

The Pros and Cons of Running a Business from Home

The Pros and Cons of running a business from home. Considering running a business from home? Read more here.

The Importance of a Business Plan

See why every start-up needs a business plan, what to include in your business plan and why. Easily draft your business plan with our free guidance.

How to Register a Business Name with Companies House: A Step-by-Step Guide for UK Entrepreneurs

Learn how to register a business name with Companies House in the UK. Step-by-step guide covering name rules, fees, documents, etc

Running a Business as a Community Interest Company

Community Interests Company. Get a detailed view of the advantages and disadvantages of running a community interests company

Running a Business as an LLP

Running a business as an LLP. Get an understanding of the LLP business structure with Grow my Acorn

Running a Limited Company in the UK

Considering forming a limited company. Read our guide to see if the Limited Company is the right business structure

Running a Sole Trader Business

Becoming a sole trader. Read our guide to becoming a sole trader and see if it is the right business structure

Running a Business Partnership

Learn how business partnerships work in the UK. Setup, taxes, liability, agreements, pros & cons

Choosing the Right Business Structure

Discover UK business structures: sole trader, partnership, LLP, Ltd, PLC, CIC & charity. Pros & cons explained