How to Improve Cash Flow

How to Improve Cash Flow: Proven Tips for UK Businesses – Improving your cash flow isn’t about guesswork; it starts with a clear, honest look at where your money is actually going. The trick is to create a detailed cash flow forecast and really get to grips with your cash conversion cycle—that’s the time it takes to turn your investments in stock, materials, and other resources back into cash from sales.

This process shines a light on what you’re doing well and, more importantly, pinpoints the costly drains that are holding you back.

Understanding Your Business Cash Flow

Before you can fix a cash flow problem, you need to see it clearly. It’s a classic trap many businesses fall into: confusing profit with cash. You can have profitable sales on paper but still run out of money if clients pay late or your big expenses are due before that revenue lands in your account.

Ditching basic spreadsheets for a real-time picture of your finances is the single most important first step you can take.

A proper cash flow analysis shows you where every pound is truly going. It’s about getting granular, spotting patterns, and asking some tough questions about how you operate. This isn’t just a number-crunching exercise; it’s the foundation for every strategic decision you’ll make to get your business on solid financial footing.

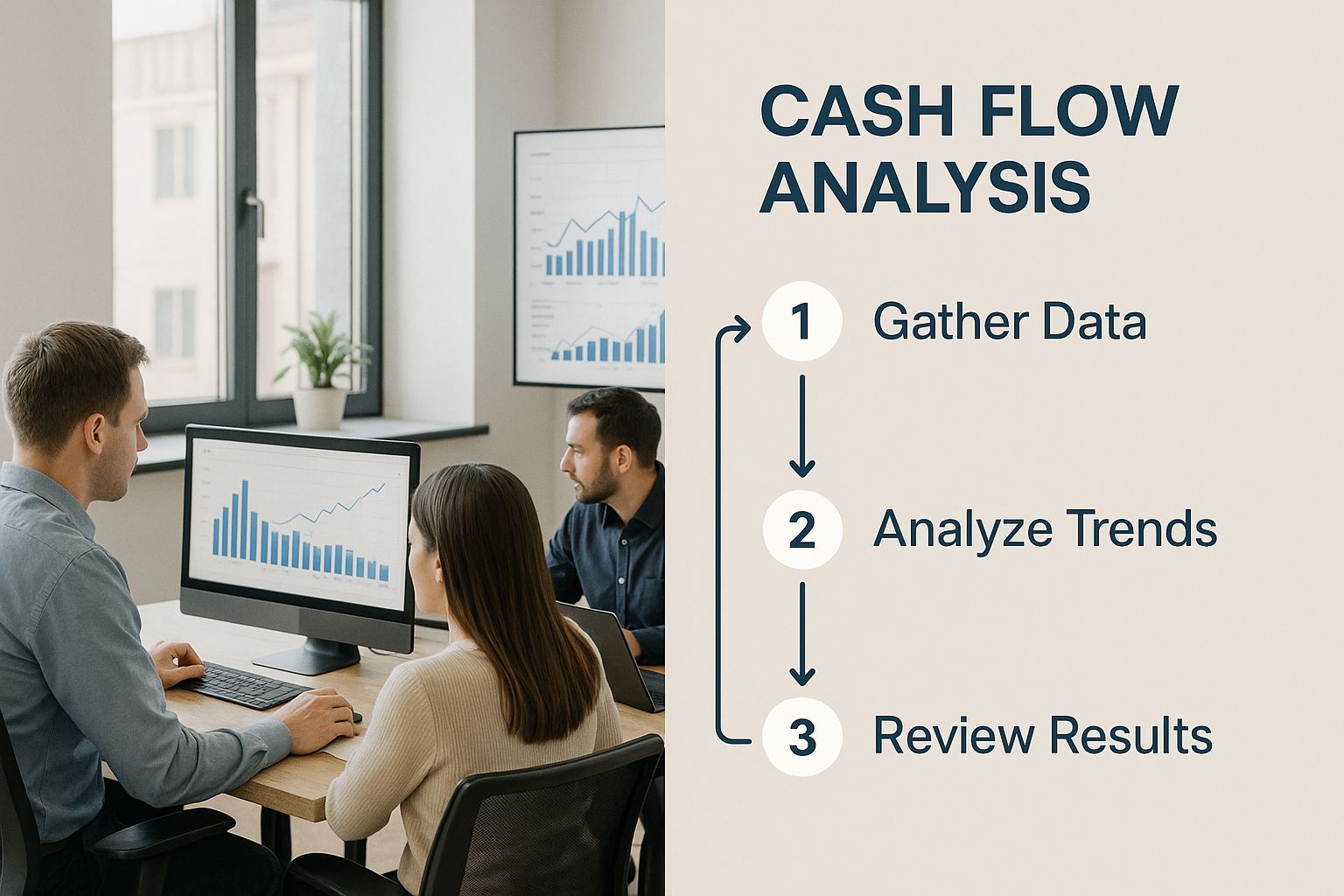

This infographic gives you a great visual guide for mapping out the process, from gathering the data to spotting the key areas for improvement.

As the breakdown shows, a full analysis isn’t just about tracking money in and money out. It’s about understanding the timing and cycles that either build up or eat away at your cash reserves.

Finding the Hidden Drains

Let’s take a small, UK-based digital marketing agency as an example. Their profit and loss statement looked pretty healthy, but they were constantly scrambling to meet payroll. It didn’t make sense until they performed a deep-dive cash flow analysis, which uncovered two significant drains.

First, they realised they were spending nearly £400 per month on overlapping software subscriptions. These were tools that did similar jobs but had been signed up by different team members over time. Second, their client acquisition spending was all wrong. They were pouring money into a marketing channel that brought in low-value, slow-paying clients, creating a massive bottleneck in their cash conversion cycle.

A cash flow statement is like a health check for your business. It tells you the story of how money moves through your company, revealing whether your operations are generating enough cash to sustain and grow.

Mapping Your Cash Conversion Cycle

Your Cash Conversion Cycle (CCC) is a metric you absolutely need to know. It measures the number of days it takes for your business to convert its investments in inventory and other resources into cash from sales. The goal is simple: make this cycle as short as possible.

To work it out, you need to understand three key parts:

- Days Inventory Outstanding (DIO): How long does it take you to sell your stock?

- Days Sales Outstanding (DSO): How long does it take you to get paid after making a sale?

- Days Payables Outstanding (DPO): How long do you take to pay your own suppliers?

For service-based businesses like our marketing agency, “inventory” is a bit different. Think of it as the time and resources they invest in a project before they can bill for it. Their analysis showed a ridiculously high DSO, driven by lenient 60-day payment terms and a casual approach to chasing overdue invoices. All their cash was tied up with clients for far too long.

Ready to start your own analysis? You can get a head start by using a professional free cashflow forecast template to organise your financial data properly.

By identifying these specific issues—overspending on software and a lengthy CCC caused by slow collections—the agency could finally create a targeted plan. This kind of foundational knowledge is essential before you can start implementing the strategies we’ll explore next.

Tightening Up Your Invoicing and Collections

If your cash flow review shows that money is consistently getting stuck with clients, you’re not alone. Getting paid on time is one of the most persistent battles for small businesses, but it’s a fight you have to win. More often than not, the culprit is a disorganised invoicing process that lets your hard-earned cash sit in someone else’s bank account.

The good news? You can build a proactive system that gets you paid faster. This isn’t about hounding clients; it’s about making it crystal clear from the start when and how they should pay you.

Making small, consistent tweaks to how you invoice and collect payments can have a massive impact on your financial stability. These changes shorten your payment cycles and put the cash you need back into your business, right where it belongs.

Refine Your Invoices from the Ground Up

Think of your invoice as the final, crucial step in your sales process. If it’s vague or confusing, it’s an open invitation for delays. Every single invoice you send needs to be professional, precise, and leave no room for questions.

I once worked with a freelance graphic designer who was constantly frustrated with late payments, with her average client taking a painful 45 days to pay up. By making a few simple tweaks, she cut that down to just 15 days.

Here’s what she changed:

- Detailed Line Items: Instead of a single line for “Logo Design,” she broke it down into “Initial Concept Development,” “Revision Round 1,” and “Final Asset Delivery.” This simple change reminded clients of the value they received at each stage.

- Clear Due Dates: Vague terms like “Payment due upon receipt” were replaced with a specific, unmissable date (e.g., “Due by 15th October 2024“).

- Multiple Payment Options: She added direct links for online card payments right next to her bank details, removing any friction that might slow a client down.

These small adjustments turned her invoices from passive requests into clear, actionable instructions. It suddenly became much easier for her clients to pay her on time.

Set Firm Payment Terms and Use Smart Incentives

Your payment terms aren’t just a suggestion; they are a core part of your business agreement. You need to discuss these terms upfront and make sure they’re clearly laid out in your contracts. If you’re unsure about the legal side of this, it’s always a good idea to get advice on how to protect your business with contracts and agreements.

A great way to nudge clients towards faster payment is by using incentives. Offering a small discount for settling up early can be surprisingly effective.

For example, offering a 2% discount if an invoice is paid within 10 days can be enough to move your bill to the top of a client’s to-do list. That small hit is often a fantastic trade-off for getting cash in the bank weeks earlier.

On the flip side, you can also implement late payment fees, as stipulated by UK law. While you should be tactful about applying them, simply having a late payment clause in your terms and conditions is a powerful deterrent against delays.

To help you decide which approach is right for your business, here’s a quick comparison of the most effective strategies.

Effective Invoice Payment Strategies Comparison

| Strategy | Description | Pros | Cons | Best For |

|---|---|---|---|---|

| Early Payment Discount | Offering a small percentage discount (1–2%) if the invoice is paid within a short window (e.g., 10 days). | Encourages prompt payment, improves cash flow, and builds goodwill with clients. | Reduces your total revenue slightly. Can be complex to track if not automated. | Businesses with healthy profit margins that want to accelerate cash flow for operational needs. |

| Late Payment Fees | Adding a penalty fee or interest for invoices that are paid after the due date, as allowed by UK law. | Deters late payments and compensates you for the delay. Reinforces the importance of deadlines. | Can damage client relationships if not handled carefully. May be difficult to enforce. | B2B service providers and businesses with clear, legally sound contracts in place. |

| Upfront Deposits / Milestone Payments | Requiring a percentage of the total fee upfront (25–50%) or billing at key project milestones. | Secures cash before work begins, reduces the risk of non-payment, and funds project costs. | May be a barrier for some new clients. Requires careful project and milestone tracking. | Project-based businesses like web design, construction, and consulting. |

| Automated Payment Reminders | Using accounting software to send automated email reminders before, on, and after the due date. | Saves time, ensures consistency, and acts as a professional, non-confrontational nudge. | Can feel impersonal if not customised. Relies on clients checking their emails. | Virtually any business, especially those with a high volume of invoices. |

| Flexible Payment Options | Offering multiple ways to pay, such as bank transfer, credit/debit card, and online payment gateways. | Removes payment friction, makes it easier for clients to pay instantly, and speeds up the process. | Card processing fees can add up. Requires setting up different payment systems. | E-commerce, freelance services, and any business dealing with online payments. |

Each strategy has its place. The key is to choose the one that best fits your business model and client relationships, ensuring your payment process is both effective and professional.

Automate and Escalate Your Collections Process

Chasing overdue invoices is a necessary evil, but it doesn’t have to be confrontational or eat up your valuable time. An automated, systematic approach ensures no invoice slips through the cracks while maintaining a professional tone.

A structured follow-up system might look like this:

- The Friendly Nudge: An automated, polite email is sent a few days before the due date.

- The Day After Reminder: Another automated email goes out the day after the invoice becomes overdue.

- The Personal Phone Call: If the invoice is a week late, a quick, friendly phone call can often resolve the issue in minutes. It’s much harder to ignore a person than an email.

- The Formal Letter: For invoices over 30 days late, a more formal letter outlining the consequences of non-payment may be necessary.

This tiered approach lets you escalate your efforts gradually. You preserve the client relationship for as long as possible while still showing that you take getting paid seriously. By combining crystal-clear invoicing, firm terms, and a structured collections process, you can systematically plug the leaks in your cash flow and build a much more resilient business.

Taking Control of Costs and Managing Expenses

Improving your cash flow isn’t just about what’s coming in; it’s about being smarter with what’s going out. A sharp eye on your expenses can free up a surprising amount of cash, giving your business the breathing room it needs to really thrive.

This isn’t about ruthless cost-slashing that stunts your growth. It’s about making deliberate, strategic financial choices. The first step is to get forensic with your bank statements and accounting software. You need to draw a clear line between your essential costs—the non-negotiables like rent, payroll, and core software—and the ‘nice-to-haves’ that have crept in over time.

Conduct a Realistic Expense Audit

An expense audit often uncovers what I call “subscription creep.” This is where lots of small, recurring charges quietly add up to a hefty monthly outgoing. Look for overlapping services, tools your team no longer uses, or premium-tier subscriptions you could easily downgrade without anyone noticing.

I saw this with a small coffee shop chain in Manchester. They did an audit and found they were paying for three different scheduling software tools across their four locations. By moving everyone onto a single, better system, they immediately saved over £150 a month. It might not sound like much, but those small wins add up fast.

The goal of an expense audit isn’t just to cut costs, but to align your spending with what actually matters. Every pound you spend should be actively contributing to your business’s health and growth.

Once you have a clear picture, you can start making targeted changes. Focus on the areas that offer the biggest returns without messing with your core operations.

Get on the Phone with Your Suppliers

Your relationships with suppliers are a two-way street, and there’s often more wiggle room than you might think. Don’t be afraid to have an open conversation with your key vendors. If you’ve been a loyal, reliable customer, they have a vested interest in keeping your business.

Try a few of these tactics:

- Bulk Discounts: Can you get a better per-unit price by placing a larger, less frequent order? This works beautifully for non-perishable goods.

- Long-Term Contracts: Some suppliers will offer a reduced rate in exchange for a longer commitment, giving you predictable costs and them guaranteed business.

- Early Payment Discounts: It feels counterintuitive when you’re trying to hold onto cash, but sometimes paying a supplier early can unlock a discount that improves your overall margin.

That same Manchester coffee shop chain provides a perfect example. They approached their main coffee bean supplier and renegotiated their contract, securing a 10% discount simply by committing to a one-year agreement. That single conversation made a huge difference to their monthly outgoings.

Lease vs Buy: Make the Smart Choice

Big-ticket items like equipment and vehicles can put a massive dent in your cash reserves. Before you make any large purchase, you absolutely have to weigh up the pros and cons of buying versus leasing.

Buying outright means you own the asset, which is great, but it ties up a huge chunk of capital that could be used for wages, marketing, or inventory. Leasing, on the other hand, means smaller, regular payments, which is much kinder to your immediate cash flow.

Think about a construction firm needing a new excavator. Buying one could cost upwards of £50,000—a massive cash outlay. Leasing it for £1,500 a month keeps that capital free for other operational needs. For any equipment that isn’t used daily or becomes outdated quickly, leasing is almost always the more cash-flow-friendly option.

Trim Your Operational Overhead

Finally, take a hard look at your day-to-day operational costs. Simple changes here can lead to substantial savings over time. Switching to energy-efficient LED lighting, encouraging double-sided printing, or upgrading old, power-hungry appliances are all practical, easy wins.

Our coffee shop chain did exactly this. They invested in new, energy-efficient espresso machines and refrigerators. While there was an initial cost, their monthly electricity bill dropped by over 20%. These mindful choices, from supplier deals to new appliances, contributed to a total 15% reduction in their monthly expenses, directly boosting their cash flow.

Managing Inventory and Supplier Payments

Getting paid faster is only half the battle. To truly get a grip on your cash flow, you need to master your outgoings with the same level of focus. How you handle supplier payments and manage stock can make or break your financial stability, giving you the power to keep cash in your business for longer.

It’s all about striking a smart balance. You have to meet your obligations and keep suppliers happy, but you also need to be strategic about when your money leaves the bank. A few small tweaks here can have a massive impact on your day-to-day cash position.

Negotiate Better Supplier Payment Terms

Never assume the payment terms a supplier offers are set in stone. If you’re a good, reliable customer, you have more leverage than you think. A simple conversation is often all it takes to agree on more favourable terms that better suit your cash flow cycle.

Your goal here is to extend your Days Payables Outstanding (DPO) – that’s the average time it takes you to pay your suppliers. A longer DPO means cash stays in your business for longer, helping you cover payroll and other operational costs before those bills come due.

For instance, if you’re currently on “Net 30” terms, why not ask to move to “Net 45” or even “Net 60”? Many suppliers will happily agree to keep a loyal customer, especially if you can offer something in return, like a slightly larger order or a longer-term commitment.

This is especially critical when you see how badly late payments are hitting UK businesses. A shocking 62% of small businesses are owed money from unpaid invoices, with the average debt sitting at a staggering £21,400 each. As you can imagine, that creates enormous cash flow pressure. You can dive deeper into the research on small business late payments in 2025.

Use Early Payment Discounts Strategically

Paying a bill early when you’re trying to hoard cash might sound counterintuitive, but sometimes it makes perfect financial sense. Many suppliers offer a discount, typically around 1-2%, for paying an invoice within, say, 10 days instead of the usual 30.

A 2% discount on a £10,000 invoice is £200 saved. It might not sound like much, but apply that across multiple suppliers and the annual savings add up, directly boosting your bottom line.

The key is to be strategic. Only jump on these discounts when you have a healthy cash reserve. It’s a bad trade-off to save a few quid if it leaves you scrambling to cover payroll. Always weigh the discount against the value of keeping that cash on hand for the full payment term.

Implement Smarter Inventory Management

If you sell physical products, your inventory is a giant cash trap. Every single item sitting on your shelves represents money you can’t use for anything else. This is where smart inventory management becomes one of your most powerful cash flow tools.

A classic and highly effective technique is Just-In-Time (JIT) inventory. The principle is simple: you order stock from suppliers only as you need it to fulfil customer orders, rather than holding huge amounts of products. This dramatically reduces the capital tied up in unsold goods and slashes your storage costs.

Here’s how to make it work:

- Dig into your sales data: Use your sales history to identify your bestsellers and which items are gathering dust. This data tells you exactly what to order more of and what to cut back on.

- Set reorder points: For your most popular products, establish automatic reorder points. This ensures you never run out of your best stuff without having to hold excessive inventory.

- Build strong supplier relationships: A JIT system lives or dies by the reliability of your suppliers. You need partners who can deliver quality goods quickly, so build strong relationships with them.

I once worked with a UK-based e-commerce retailer selling handmade jewellery. They dug into their sales data and realised 80% of their revenue came from just 20% of their products. By adopting a JIT approach for their less popular items and only keeping their bestsellers in stock, they freed up thousands of pounds and cut their storage costs by half. It’s a perfect example of how a small change can unlock so much cash.

Using Finance to Bridge Cash Flow Gaps

Even the most profitable business can hit a cash flow squeeze. It happens. You might land a huge new order that requires a big upfront investment in materials, or perhaps a key client unexpectedly delays a large payment.

When these moments strike, turning to external finance isn’t a sign of failure. Far from it. It’s a strategic tool that allows you to bridge temporary gaps, protect your relationships, and even seize growth opportunities you’d otherwise have to pass up. The trick is to understand what’s out there and pick the right tool for the job.

Traditional Tools for Predictable Needs

When you have a clear, long-term purpose for needing funds, traditional options like a business loan or an overdraft often make the most sense. They bring a sense of structure and predictability, which is exactly what you want for planned investments.

A business loan is perfect for a one-off, significant expense where you can see a clear return on your investment down the line. Think about buying a crucial piece of machinery, funding a major office refurbishment, or covering the costs of launching a new product. You get a lump sum upfront and repay it in fixed monthly instalments, making it easy to budget for. To make sure everything is crystal clear, using a free loan agreement template can provide peace of mind for everyone involved.

A business overdraft, on the other hand, is more of a safety net attached to your current account. It’s really designed for those short-term working capital hiccups, like covering wages the week before a big client payment is due to land. You only pay interest on the amount you actually use, making it a flexible buffer for minor, unexpected shortfalls.

A Quick Look at the Current Climate: Recent data shows just how vital finance facilities are for UK SMEs. In the first quarter of this year, overdraft approvals for small businesses hit their highest point since mid-2020, giving a much-needed boost to sectors like manufacturing and construction. Interestingly, though, businesses are still cautious; utilisation rates are sitting below 50%, which suggests a careful balancing act between needing liquidity and wanting to avoid unnecessary debt.

Flexible Alternatives for Modern Challenges

Sometimes, the traditional options just don’t fit the bill. Your needs might be more immediate or tied directly to the rhythm of your sales cycle. This is where a new wave of flexible financing solutions has really come into its own, offering a more dynamic way to manage your cash flow.

Two of the most powerful options I see businesses using are:

- Invoice Financing: This is an absolute game-changer for businesses with long payment terms. It lets you unlock the cash that’s tied up in your unpaid invoices. Instead of waiting 30, 60, or even 90 days for a client to pay up, a finance company can advance you up to 90% of the invoice value almost immediately.

- Business Line of Credit: Think of this as a more formal, standalone version of an overdraft. You get access to a pre-approved pot of funds that you can draw from whenever you need it, and you only pay interest on what you borrow. It’s ideal for managing unpredictable expenses or jumping on opportunities that pop up out of the blue.

A Real-World Example in Action

Let’s picture a small construction company in Leeds that’s just won a large commercial contract. It’s a six-month project, with payments staged at key milestones. Here’s the problem: they need to pay for a mountain of materials and cover a larger wage bill right now, but the first project payment is still eight weeks away.

Putting all those materials on a trade account would strain supplier relationships, and applying for a traditional loan would be too slow and rigid for this specific, short-term need.

This is the perfect scenario for invoice financing. They can submit their first project invoice to a finance provider and get the bulk of the cash in their account within a couple of days. That injection of funds means they can buy everything they need and meet payroll without breaking a sweat. When the client eventually pays the full invoice, the finance company takes its fee, and the construction firm gets the rest.

They’ve successfully bridged the gap, kept the project on track, and maintained great relationships with their suppliers. No stress, no drama.

UK SME Financing Options at a Glance

To help you get a clearer picture, here’s a quick breakdown of the most common financing options and when they might be the right fit for your business.

| Financing Option | How It Works | Ideal For | Key Consideration |

|---|---|---|---|

| Business Loan | A lump sum of cash repaid over a fixed term with regular interest payments. | Large, planned one-off investments like purchasing new equipment or property. | Requires a strong business plan and can take time to get approved. |

| Business Overdraft | An agreed-upon limit to overdraw your business current account. | Covering very short-term, minor cash shortfalls, like payroll before a payment arrives. | Interest rates can be high, and the facility can be recalled by the bank. |

| Invoice Financing | A provider advances you a percentage of your unpaid invoices’ value. | Businesses with long payment cycles (e.g., B2B services, construction, manufacturing). | The fee reduces your profit margin on the invoice. |

| Line of Credit | A flexible, pre-approved borrowing facility you can draw from as needed. | Managing fluctuating working capital needs or seizing unexpected opportunities. | Can encourage reliance on debt if not managed carefully; interest accrues on the drawn balance. |

Ultimately, choosing the right financing is all about matching the solution to the specific problem you’re facing. By understanding these tools, you can empower your business to navigate any temporary dip and confidently invest in its future.

Your Top Cash Flow Questions Answered

When you’re trying to get a handle on your cash flow, the same urgent questions always seem to pop up. Business owners need straight answers to their most immediate worries, so let’s tackle the common ones with clear, practical advice you can use right away.

Getting on top of cash flow means being able to solve problems as they appear. Understanding these core ideas is the key to making confident financial decisions and building a more resilient business.

What Is the Single Fastest Way to Improve Cash Flow?

When you need cash now, the quickest win is almost always to chase your largest and oldest overdue invoices. This isn’t about setting up a fancy new system; it’s about focused, immediate action. Your accounts receivable ledger is full of cash that is rightfully yours, and a few phone calls can often unlock it within days.

Imagine a small IT support company with five overdue invoices. Instead of sending another generic reminder email to everyone, the owner should pick out the single biggest invoice that’s more than 30 days late. A personal, polite phone call to that client’s finance department is far more effective and can often get you an immediate payment commitment.

Don’t underestimate the power of picking up the phone. A simple call can cut through the noise of an overflowing inbox and resolve a payment issue in minutes, injecting much-needed cash straight back into your business.

How Often Should I Check My Cash Flow?

How often you review your cash flow depends on your type of business, but a solid rule of thumb is to check it at least weekly. A monthly review is the absolute bare minimum, but in a fast-moving business, a month is more than enough time for a small issue to spiral into a full-blown crisis.

A weekly check-in doesn’t have to be a deep, hours-long analysis. It can be a simple 15-minute review to:

- See what payments have actually landed in your account.

- Check which new invoices have become overdue.

- Review your upcoming bills for the next seven days.

- Glance at your bank balance to make sure you have enough buffer.

For businesses with tighter margins or big seasonal swings, like a restaurant or a retail shop, a daily cash reconciliation is essential. This constant monitoring lets you spot negative trends early and act before your cash reserves run dry.

Can My Business Be Profitable But Still Have No Cash?

Yes, absolutely. This is one of the most dangerous—and common—misunderstandings in business finance. It’s a trap that catches many successful, growing businesses by surprise, often called profitless prosperity. Profit and cash are two very different things, and confusing them can be fatal.

Profit is an accounting calculation on paper. It’s the difference between your revenue and your expenses over a period (e.g., Revenue of £50,000 – Expenses of £30,000 = £20,000 Profit). The crucial point is that this calculation doesn’t care when you get paid or when you have to pay your bills.

Here’s a real-world scenario:

A growing marketing agency lands a massive £100,000 project. On paper, they look incredibly profitable. But their payment terms are “Net 90,” meaning they won’t see a penny of that cash for three months. In the meantime, they still have to pay their staff, their rent, and their software subscriptions every single month.

The business is profitable, but because all its cash is tied up waiting to be collected, it could easily run out of money to cover its immediate costs. This is why managing cash flow—the actual movement of money in and out of your bank account—is just as important, if not more so, than simply turning a profit.

At Grow My Acorn, we’re dedicated to giving you the information and advice you need to build a financially healthy business. For more guides and resources to help you succeed, visit us at growmyacorn.co.uk.

More Topics

What is invoice factoring: A Clear Guide to Faster Cash Flow

Discover what is invoice factoring and how it unlocks fast cash flow for your business with simple examples and practical steps.

12 Profitable Self Employment Ideas to Start in 2025

Discover 12 practical self employment ideas you can launch this year. Our guide covers startup costs, skills, and

How to Delegate Effectively: Master Your Team Productivity

Discover how to delegate effectively with practical tips to boost team productivity, empower others, and drive better results.

How to Build an Email List from Scrath

Learn how to build an email list with our practical guide. Discover actionable strategies and expert tips to grow an audience that converts.

How to Improve Employee Retention

Discover how to improve employee retention with actionable strategies on leadership, compensation, and culture

Streamlining business processes: Boost efficiency today

Discover how streamlining business processes can unlock efficiency and drive growth with practical, actionable steps.

marketing tips for small business: 5 quick wins

Uncover marketing tips for small business that boost ROI with 5 practical strategies you can implement this week

what is professional indemnity insurance? A quick guide

what is professional indemnity insurance: learn what it covers, who needs it, and how to choose the right PI policy for your business.

10 Actionable Marketing Tips for Small Businesses in 2025

Discover 10 practical marketing tips for small businesses. Boost your growth with budget-friendly strategies for SEO,

10 Profitable Business Ideas UK from Home for 2025

Discover 10 practical profitable business ideas UK from home. This guide covers startup costs, income potential,

What Is a Break Even Analysis Explained

What is a break even analysis? Learn how to calculate it and use this simple tool to make smarter financial decisions for your business.

How to Create a Cash Flow Forecast That Works

Learn how to create a cash flow forecast with this practical guide. We cover predicting inflows, mapping outflows,

How to Write a Business Proposal That Wins Clients

Learn how to write a business proposal that actually wins clients. Offering advice and real-world examples

What Is Equity Dilution for Founders

Understand what is equity dilution and how it impacts your startup. Our guide explains cap tables, funding rounds

How to Conduct Competitor Analysis That Drives Growth

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

How to Register a Business in the UK Your Complete Guide

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

12 Best Ways to Advertise Your Business in 2025

12 Best Ways to Advertise Your Business Discover the best ways to advertise your business

Small Business Accounting Basics Made Simple

Master small business accounting basics with our guide. Learn bookkeeping, financial statements, and tax

Business Exit Strategy Planning Done Right

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Find Business Partners That Actually Fit

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

High Street vs Digital Business Banking

Compare High Street vs Digital Business Banking for start-ups. Discover the pros and cons of business banking

10 Crucial Pieces of Business Advice for Startups

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

How to Scale a Business The Right Way

Learn how to scale a business with proven, real-world strategies. The complete guide

A Board Meeting Agenda Template That Actually Works

Tired of unproductive meetings? Use our board meeting agenda template to drive focus, ensure compliance

Sole Trader Tax Deductions

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Build Business Credit for Your UK Business

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

What Is a Business Model Canvas?

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Improve Customer Service A UK Business Guide

Discover how to improve customer service with actionable strategies for UK businesses

Dealing with Difficult Clients: Top Strategies for Success

Dealing with difficult clients isn’t about winning arguments. Learn how to deal with difficult clients.

Business Plan Executive Summary Examples: 8 Inspiring Samples

How to professionally prepare your business plan executive summary along with practical examples.

Your Guide to a Business Risk Management Framework

Build a robust business risk management framework with our free online guidance.

Social Media Marketing for Small Business

Social Media Marketing for Small Business Free Expert Guidance from Grow My Acorn the ultimate free resource

10 Powerful Customer Retention Strategies for 2025

Discover 10 actionable customer retention strategies with real examples. Learn how to boost loyalty,

How to Grow a Business The Right Way

How to Grow a Business The Right Way grow your business the right way with free expert advice

Proven Marketing Strategies for Small Businesses

Get your marketing strategy off to a flying start with our proven strategies guaranteed to deliver measurable results.

Sole Trader vs Limited Company UK Guide

Choose the right business structure. Understand the differences, benefits and pitfalls. Sole Trader? Limited Company?

How to Start a Business in the UK

How to start a business in the UK – Your handy free expert guide on how to start a business in the UK

How to Protect Your Business with Contracts and Agreements

Learn how to protect your business with contracts and agreements. A practical guide for startups

Taking the Leap: The Ultimate Guide to Hiring Your First Employee

Thinking of hiring your first employee? Take a look at our handy guide to understand when and how to recruit.

10 Proven Low-Cost Marketing Strategies for Startups

10 proven low costs marketing strategies which you can implement today to grow your business.

How Much Does It Really Cost to Start a Small Business

Wondering how much it costs to start a small business in the UK? Discover the real start up expenses for entrepreneurs,

Top 20 Home Based Business Ideas

Looking for the best home based business ideas? Discover 20 profitable ways to start a business from home

The Pros and Cons of Running a Business from Home

The Pros and Cons of running a business from home. Considering running a business from home? Read more here.

The Importance of a Business Plan

See why every start-up needs a business plan, what to include in your business plan and why. Easily draft your business plan with our free guidance.

How to Register a Business Name with Companies House: A Step-by-Step Guide for UK Entrepreneurs

Learn how to register a business name with Companies House in the UK. Step-by-step guide covering name rules, fees, documents, etc

Running a Business as a Community Interest Company

Community Interests Company. Get a detailed view of the advantages and disadvantages of running a community interests company

Running a Business as an LLP

Running a business as an LLP. Get an understanding of the LLP business structure with Grow my Acorn

Running a Limited Company in the UK

Considering forming a limited company. Read our guide to see if the Limited Company is the right business structure

Running a Sole Trader Business

Becoming a sole trader. Read our guide to becoming a sole trader and see if it is the right business structure

Running a Business Partnership

Learn how business partnerships work in the UK. Setup, taxes, liability, agreements, pros & cons

Choosing the Right Business Structure

Discover UK business structures: sole trader, partnership, LLP, Ltd, PLC, CIC & charity. Pros & cons explained