How to Create a Cash Flow Forecast That Works

How to Create a Cash Flow Forecast That Works – Creating a cash flow forecast isn’t as complicated as it sounds.It breaks down into three core stages: pulling together your financial data, projecting your inflows and outflows, and then analysing the results to see what’s coming down the track.

Think of it as turning historical data into a forward-looking financial roadmap. It’s a process that every business owner needs to master.

Why a Cash Flow Forecast Is Your Secret Weapon

Managing money can often feel like you’re constantly putting out fires. A solid cash flow forecast is more than just a spreadsheet; it’s your business’s early warning system and strategic guide. For UK businesses facing today’s economic pressures, it’s an absolutely essential tool.

It’s like having a financial crystal ball that helps you make informed, proactive decisions rather than reactive ones. With a clear picture of your future cash position, you can:

- Anticipate Cash Shortages: Spot potential dips in your bank balance weeks or even months in advance. This gives you precious time to arrange an overdraft, chase late payments, or delay a non-essential purchase.

- Seize Growth Opportunities: Confidently decide when to hire your next team member, invest in new equipment, or launch a big marketing campaign because you know the cash will be there to cover it.

- Improve Supplier Relationships: Ensure you always have the funds to pay suppliers on time. This isn’t just good manners; it strengthens your business reputation and can even give you better negotiating power for future deals.

Before we get into the nuts and bolts of building your forecast, it helps to understand the core steps involved. This table gives you a quick overview of the journey ahead.

Quick Guide to Cash Flow Forecasting Steps

| Stage | Key Action | Primary Goal |

|---|---|---|

| 1. Gather Your Data | Collect historical bank statements, sales records, and expense reports. | To establish a reliable baseline of your past financial performance. |

| 2. Choose a Template | Select a spreadsheet or software that fits your business needs. | To provide a structured framework for your forecast, saving time and effort. |

| 3. Project Inflows | Estimate future sales, client payments, and other incoming cash. | To build a realistic picture of the money coming into your business. |

| 4. Project Outflows | Forecast all expected expenses, from rent and payroll to supplier costs. | To map out all the money leaving your business each month. |

| 5. Analyse the Results | Identify potential cash gaps or surpluses and plan accordingly. | To turn your forecast into actionable insights and strategic decisions. |

As you can see, the process is logical and moves from what you know (your history) to what you can predict (your future).

A Real-World Scenario

Imagine a small retail business in Manchester. They’re doing well, but rising supplier costs are eating into their profits and making cash flow unpredictable. Without a forecast, a sudden, larger-than-expected invoice could land, leaving them scrambling to cover payroll.

This is an incredibly common situation, especially since nearly 47% of UK small businesses report cash flow issues amid rising costs. You can learn more about the challenges facing UK SMEs from recent survey data.

A cash flow forecast transforms this potential crisis into a manageable challenge. By mapping out expected sales against rising supplier payments, the owner can see the looming shortfall two months ahead.

This foresight is a game-changer. It allows them to act strategically. They might delay a non-essential stock purchase or run a targeted promotion to boost sales in the preceding month.

Instead of panicking, they are in control. This is exactly why mastering your cash flow is non-negotiable. Now, let’s dive into how you can build your own.

Gathering the Right Financial Data

A forecast is only as reliable as the data you build it on. It’s a simple truth, but one that’s easy to forget. Before you can even think about predicting the future, you need a crystal-clear understanding of your business’s financial past. This means getting your hands on specific documents to create an accurate baseline.

Think of this part of the process as assembling the ingredients for a recipe. Without the right components, the final dish just won’t work. Your goal is to build a complete financial picture, leaving no stone unturned.

Your Essential Data Checklist

First things first, you’ll need to pull together a few key sources of information. Most of this should be sitting in your accounting software, your online banking portal, or even in physical files if you’re more old-school.

Here’s what you should be looking for:

- Historical Bank Statements: Go back at least six to twelve months. This gives you a solid overview of all the cash that’s actually moved in and out of your business.

- Sales Records and Invoices: These documents detail who owes you money (accounts receivable) and when those payments are due, which is crucial for projecting your cash inflows.

- Supplier Bills and Expense Reports: This is the other side of the coin, showing who you owe money to (accounts payable). It includes everything from raw materials and stock to utility bills and software subscriptions.

- Loan and Credit Card Statements: Don’t forget these. Make sure you have the repayment schedules for any loans, overdrafts, or credit card balances.

Once you have these documents, it’s time to get them organised. A great way to get started is by using a pre-built spreadsheet. For a solid foundation, you can download a free cashflow forecast template to help structure your data logically.

A Practical Example: A Digital Marketing Agency

Let’s imagine a digital marketing agency in Leeds. Their income is a tricky mix of fixed monthly retainers and variable one-off project fees, which makes forecasting a real challenge. On top of that, their client payment schedules are unpredictable—some pay on time, while others seem to always stretch invoices to 60 or 90 days.

To build a forecast that’s actually useful, the agency owner needs to dig deep and:

- Track That Variable Income: They can’t just look at when an invoice is sent. They must analyse their sales pipeline to realistically estimate when new project payments will actually land in the bank.

- Identify All The Overheads: It’s not just about the big costs like rent and salaries. They need to list every single recurring software subscription—from project management tools to social media schedulers. These small amounts really add up.

- Account for Payment Delays: By reviewing their accounts receivable history, they can spot which clients consistently pay late. This allows them to adjust their inflow projections to reflect reality, not wishful thinking.

A common mistake is being too optimistic. Ignoring historical data, like seasonal sales dips or those chronically late-paying clients, will create a forecast that looks great on paper but falls apart in the real world.

By diligently gathering and reviewing this data, the agency can move from pure guesswork to an evidence-based approach. They now have a clean, complete, and honest financial picture, which is the only foundation you want when building a powerful cash flow forecast.

How to Accurately Project Your Cash Inflows

Predicting the money coming into your business is both an art and a science. A reliable forecast isn’t about wishful thinking; it’s about blending historical data with realistic assumptions about the future. You don’t need complex formulas, just practical methods for figuring out when cash will actually land in your bank account.

This means looking at your past performance, your current sales pipeline, and what’s happening in the wider market to build a believable picture of your future income. Getting this right is the cornerstone of a cash flow forecast you can actually depend on.

Start with Your Sales Forecast

Your main source of cash is almost always your sales revenue. The trick here is to be conservative and base your projections on solid evidence, not just blind optimism. The best way to do this is to break down your sales streams for a much clearer picture.

Understanding what drives your cash flow is critical. In the UK, this often comes down to sales volume, payment terms, and pricing strategies, all while navigating a shaky economic climate. Research shows many UK businesses are grappling with cost inflation and shifting consumer habits. One outlook suggests that relatively strong wage growth is what’s propping up household spending—and therefore business revenues. Knowing this helps you set realistic assumptions for sales receipts and nail down your inflow estimates. You can dive into the full economic and fiscal outlook from the OBR for more detail.

Let’s take a catering company as an example. Their income isn’t one simple stream; it’s a mix of different activities, each with its own payment cycle.

To forecast properly, they’d need to:

- List Confirmed Bookings: Start with the money that’s practically guaranteed. They have deposits for three weddings (£4,500 total) and two corporate events (£3,000 total) next quarter. This income is highly probable.

- Estimate Daily Sales: They also run a small café. Looking at past data, they know sales dip in January but spike during local summer festivals. They can project daily takings based on last year’s figures, tweaking for any known changes. For example, they might forecast £8,000 for a typical month, but £12,000 in a festival month.

- Analyse the Sales Pipeline: They’ve sent out quotes for five other large events totalling £25,000. Based on their historical conversion rate of 40%, they can realistically forecast that two of those will turn into confirmed bookings, adding another £10,000 to their projection.

This multi-pronged approach gives you a far more robust projection than a simple, single-figure guess.

Account for Other Income Sources

Sales revenue is the main act, but it might not be the only cash coming through the door. Forgetting about other inflows can seriously skew your forecast and give you a false sense of your financial health.

Remember, a cash flow forecast tracks all cash movements. This includes non-sales income that can significantly impact your bank balance, even if it’s just a one-off.

Don’t forget to include these potential cash injections:

- Asset Sales: Are you planning to sell an old delivery van or some unused kitchen equipment? The proceeds from that sale are a one-time cash inflow. For example, you might budget for receiving £2,500 in May from selling a surplus coffee machine.

- Loans or Investment: If you’ve secured a business loan or received funds from an investor, that money needs to be logged in the month it arrives. This could be a £20,000 director’s loan in September to fund expansion.

- VAT Refunds: If you’re expecting a VAT refund from HMRC, this is a direct cash inflow that should be included in your forecast for the month you expect to receive it. For instance, a £1,800 refund due in July.

By combining detailed sales projections with a thorough account of all other potential income, you build a comprehensive and believable picture of your future cash position. This sets you up perfectly for the next stage: forecasting your outflows.

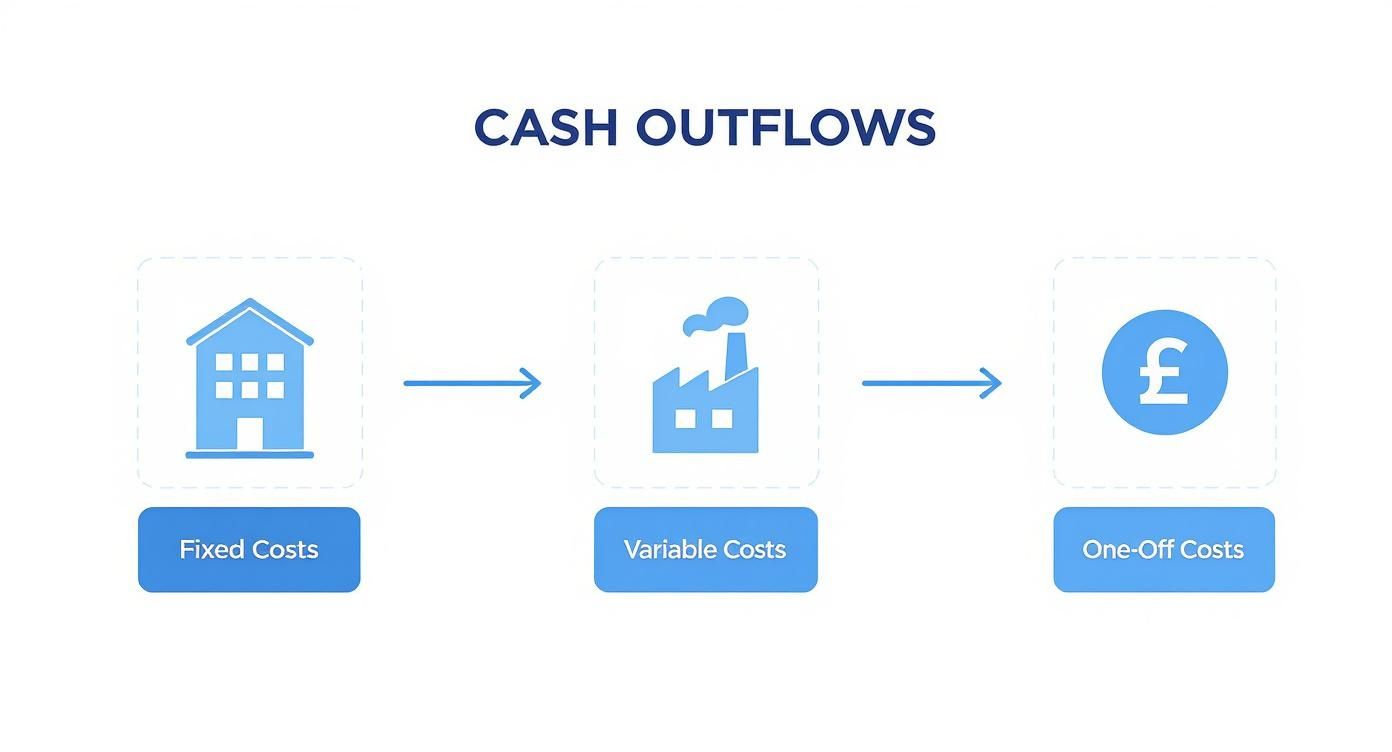

Mapping Every Business Cash Outflow

Knowing where your money is going is just as vital as knowing where it’s coming from. An accurate forecast hinges on systematically identifying and categorising every single business expense. If you miss even the small outflows, you can end up with a dangerously misleading financial picture.

To get this right, you need to break your expenses down into two main groups: fixed costs and variable costs. This distinction is critical because it helps you understand which expenses are predictable and which will fluctuate as your business activity changes.

Separating Fixed and Variable Costs

First up, let’s tackle fixed costs. These are the predictable, recurring expenses that don’t change month to month, no matter how many products you sell or services you deliver. They form the financial bedrock of your business.

Think of them as your baseline operating expenses:

- Rent for your office, workshop, or retail space (£1,200 per month)

- Salaries for your permanent staff (£5,000 per month)

- Insurance premiums (£150 per month)

- Software subscriptions (like your accounting software or CRM – £100 per month)

- Loan repayments with a fixed interest rate (£450 per month)

Next are your variable costs. These expenses move in direct proportion to your sales and production. When business is booming, these costs go up; when things slow down, they fall. Forecasting these accurately means linking them directly to your sales projections.

The real power of a cash flow forecast comes from understanding the relationship between your variable costs and your revenue. This insight allows you to predict your profitability at different sales levels and make smarter decisions about pricing and production.

A Practical Example: A Small Manufacturing Firm

Let’s picture a small firm in Sheffield that manufactures custom furniture. Their monthly fixed costs are straightforward and include £2,500 for workshop rent, £6,000 in salaries, and £300 for insurance and software. This gives them a predictable baseline of £8,800 going out every single month.

Their variable costs, however, are a different story. They change with every order they receive. These include things like:

- Raw materials such as timber and fabric (e.g., £200 per table)

- Wages for temporary workshop staff hired during busy periods (e.g., £1,000 for an extra person in a peak month)

- Delivery costs for finished pieces (e.g., £50 per table)

- Sales commissions paid to their sales agent (e.g., 5% of the sale price)

If they project selling 20 tables in April, they can estimate the timber cost will be around £4,000. But if they forecast a busier May with 30 tables, that cost rises to £6,000. It’s this direct link that turns the forecast into a dynamic tool for managing your resources.

If you’re new to this, getting a handle on these concepts is a great first step. Our guide on small business accounting basics provides a solid foundation.

Don’t Forget Significant One-Off Payments

Finally, a common pitfall is forgetting about large, infrequent expenses that can drain your cash reserves without warning. These aren’t your regular monthly outflows, but they absolutely must be included in your forecast to avoid nasty surprises.

Make sure you map out these less frequent but significant payments:

- Quarterly VAT payments to HMRC (e.g., a £4,500 payment due in July)

- Annual corporation tax bills (e.g., a £6,000 liability to be paid in October)

- Major equipment purchases or repairs (e.g., a planned £3,000 investment in a new saw in August)

- Deposits for new premises or significant stock orders

By meticulously mapping out all three types of outflows—fixed, variable, and significant one-offs—you create a comprehensive and realistic view of where your money is going. This complete picture is essential for the next step: bringing your cash flow forecast to life.

Bringing Your Cash Flow Forecast to Life

You’ve gathered the data and mapped out your inflows and outflows. Now it’s time for the magic to happen—turning all those numbers into a powerful tool that guides your business decisions. This is where you move beyond simple data entry and start to really understand what the future holds for your business’s bank balance.

The goal here is to transform a static report into a dynamic guide. You’ll be able to spot cash gaps weeks or months in advance and, just as importantly, identify surplus periods that are perfect for reinvestment or growth.

Calculating Your Net Cash Flow

At its heart, the calculation for each period—usually a month—is beautifully simple. It’s just the difference between all the cash coming in and all the cash going out.

Net Cash Flow = Total Cash Inflows – Total Cash Outflows

Let’s take a freelance graphic designer as an example. Say they project £5,000 in client payments (inflows) for July. They also anticipate £1,500 in expenses (outflows) for things like software subscriptions, co-working space rent, and a tax provision. Their net cash flow for the month is a healthy £3,500. A positive figure like this means more cash came in than went out, strengthening their financial position.

A negative net cash flow isn’t always a red flag, especially if it’s planned. It might be down to a large, one-off investment like buying a new high-spec laptop for £2,000 in a month with only £1,500 of inflows. The key is that your forecast makes you aware of it in advance, turning a potential shock into a strategic decision.

This visual breaks down the different types of cash outflows you’ll be subtracting from your inflows.

Getting a clear handle on what’s fixed versus what’s variable is crucial for making your calculations as accurate as possible.

From Static Report to Strategic Tool

Your forecast really proves its worth when you start using it for scenario planning. After all, business is never as predictable as we’d like. Answering those “what if?” questions is what separates basic bookkeeping from smart, forward-thinking financial management.

This is where you model different possibilities to see how resilient your cash flow really is.

Think about some common business curveballs:

- What happens if a major client pays their invoice 30 days late?

- What’s the impact if your key raw material costs suddenly jump by 10%?

- If a new competitor launches a price war and your sales dip by 15%, what does your closing bank balance look like in three months?

By running these scenarios, you can build contingency plans. If you see a potential cash shortfall on the horizon in your “worst-case” model, you now have the time to do something about it. Maybe you chase invoices more proactively, delay a non-essential purchase, or look into a flexible credit facility.

Scenario Planning Example Impact on Monthly Cash Flow

To make this tangible, let’s look at how a single event—a major client delaying a £5,000 payment by one month—could ripple through your forecast. Assume your opening balance is £8,000 and other inflows are £3,000, with outflows at £4,000.

| Scenario | Projected Inflow (£) | Projected Outflow (£) | Net Cash Flow (£) | Closing Balance (£) |

|---|---|---|---|---|

| Best-Case | 8,000 | 4,000 | 4,000 | 12,000 |

| Expected | 8,000 | 4,000 | 4,000 | 12,000 |

| Worst-Case | 3,000 | 4,000 | -1,000 | 7,000 |

As you can see, in the worst-case scenario, the delayed payment pushes the business into a negative net cash flow for the month, significantly reducing the closing bank balance. Having this foresight allows you to take action before the problem hits.

Exploring different options is a powerful exercise. For practical strategies, our guide on how to improve cash flow offers a great starting point.

This proactive approach turns your forecast from a passive document into an active tool for managing risk, giving your business the resilience it needs to handle whatever comes its way.

Got Questions? We’ve Got Answers

Even with the best plan, you’re bound to have questions when you first dive into cash flow forecasting. That’s perfectly normal. Getting a handle on these common queries will not only boost your confidence but also make sure you’re getting real value from the effort you put in.

Let’s walk through some of the questions I hear most often from business owners.

How Often Should I Update My Forecast?

The honest answer? It depends on how stable your business is.

For most small businesses, a monthly update is the sweet spot. This rhythm gives you a chance to look back at what actually happened last month, compare it to your predictions, and then sharpen your forecast for the coming months.

However, if your business is going through a period of big change—maybe you’re launching a new product or the market’s gone a bit wobbly—you might want to switch to weekly updates. The trick is to treat your forecast as a living, breathing document. It’s not something you do once and then file away.

The real magic isn’t just in updating the numbers. It’s about understanding the ‘why’ behind the differences. If sales were 20% lower than you projected, was it a market downturn, a competitor’s big promotion, or something that happened internally? That analysis is where the real learning happens.

Can I Just Use My Accounting Software for This?

Absolutely, and for many businesses, it’s a great way to start.

Modern accounting software like Xero, QuickBooks, and Sage often have built-in tools for cash flow forecasting. Their biggest advantage is pulling in your financial data automatically. This saves a ton of time on manual entry and dramatically cuts down the risk of errors.

- For simpler businesses: The built-in tools are often more than enough to get a clear picture.

- For more complex businesses: You might find you still prefer a dedicated spreadsheet. It gives you total control to build custom formulas, run different “what-if” scenarios, and tailor it exactly to your needs.

What’s the Difference Between a Cash Flow Forecast and a P&L?

This is a crucial distinction, and one that trips a lot of people up.

A Profit & Loss (P&L) statement tells you about your profitability. It matches your revenues against the expenses you incurred to earn them over a certain period. Think of it as your performance scorecard.

A cash flow forecast, on the other hand, tracks the actual cash moving in and out of your bank account. It’s all about liquidity—the cash you have on hand to pay the bills.

Here’s a practical example:

You send a £5,000 invoice to a client in March. Your P&L for March will show that £5,000 as revenue, making your business look profitable. But what if the client doesn’t actually pay you until May? That cash won’t show up in your bank account—and therefore your cash flow forecast—until May.

This timing gap is exactly why a profitable business on paper can still run out of cash.

Ready to take control of your business finances with expert advice and practical tools? At Grow My Acorn, we provide the resources you need to turn financial data into strategic decisions. Explore our insights and guides at https://growmyacorn.co.uk.

More Topics

What is invoice factoring: A Clear Guide to Faster Cash Flow

Discover what is invoice factoring and how it unlocks fast cash flow for your business with simple examples and practical steps.

12 Profitable Self Employment Ideas to Start in 2025

Discover 12 practical self employment ideas you can launch this year. Our guide covers startup costs, skills, and

How to Delegate Effectively: Master Your Team Productivity

Discover how to delegate effectively with practical tips to boost team productivity, empower others, and drive better results.

How to Build an Email List from Scrath

Learn how to build an email list with our practical guide. Discover actionable strategies and expert tips to grow an audience that converts.

How to Improve Employee Retention

Discover how to improve employee retention with actionable strategies on leadership, compensation, and culture

Streamlining business processes: Boost efficiency today

Discover how streamlining business processes can unlock efficiency and drive growth with practical, actionable steps.

marketing tips for small business: 5 quick wins

Uncover marketing tips for small business that boost ROI with 5 practical strategies you can implement this week

what is professional indemnity insurance? A quick guide

what is professional indemnity insurance: learn what it covers, who needs it, and how to choose the right PI policy for your business.

10 Actionable Marketing Tips for Small Businesses in 2025

Discover 10 practical marketing tips for small businesses. Boost your growth with budget-friendly strategies for SEO,

10 Profitable Business Ideas UK from Home for 2025

Discover 10 practical profitable business ideas UK from home. This guide covers startup costs, income potential,

What Is a Break Even Analysis Explained

What is a break even analysis? Learn how to calculate it and use this simple tool to make smarter financial decisions for your business.

How to Write a Business Proposal That Wins Clients

Learn how to write a business proposal that actually wins clients. Offering advice and real-world examples

What Is Equity Dilution for Founders

Understand what is equity dilution and how it impacts your startup. Our guide explains cap tables, funding rounds

How to Conduct Competitor Analysis That Drives Growth

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

How to Register a Business in the UK Your Complete Guide

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

12 Best Ways to Advertise Your Business in 2025

12 Best Ways to Advertise Your Business Discover the best ways to advertise your business

Small Business Accounting Basics Made Simple

Master small business accounting basics with our guide. Learn bookkeeping, financial statements, and tax

Business Exit Strategy Planning Done Right

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Find Business Partners That Actually Fit

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

High Street vs Digital Business Banking

Compare High Street vs Digital Business Banking for start-ups. Discover the pros and cons of business banking

10 Crucial Pieces of Business Advice for Startups

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

How to Scale a Business The Right Way

Learn how to scale a business with proven, real-world strategies. The complete guide

A Board Meeting Agenda Template That Actually Works

Tired of unproductive meetings? Use our board meeting agenda template to drive focus, ensure compliance

Sole Trader Tax Deductions

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Build Business Credit for Your UK Business

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

What Is a Business Model Canvas?

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Improve Customer Service A UK Business Guide

Discover how to improve customer service with actionable strategies for UK businesses

Dealing with Difficult Clients: Top Strategies for Success

Dealing with difficult clients isn’t about winning arguments. Learn how to deal with difficult clients.

Business Plan Executive Summary Examples: 8 Inspiring Samples

How to professionally prepare your business plan executive summary along with practical examples.

Your Guide to a Business Risk Management Framework

Build a robust business risk management framework with our free online guidance.

How to Improve Cash Flow: Proven Tips for UK Businesses

Learn how to improve cash flow with actionable strategies for UK businesses. Master invoicing, managing expenses

Social Media Marketing for Small Business

Social Media Marketing for Small Business Free Expert Guidance from Grow My Acorn the ultimate free resource

10 Powerful Customer Retention Strategies for 2025

Discover 10 actionable customer retention strategies with real examples. Learn how to boost loyalty,

How to Grow a Business The Right Way

How to Grow a Business The Right Way grow your business the right way with free expert advice

Proven Marketing Strategies for Small Businesses

Get your marketing strategy off to a flying start with our proven strategies guaranteed to deliver measurable results.

Sole Trader vs Limited Company UK Guide

Choose the right business structure. Understand the differences, benefits and pitfalls. Sole Trader? Limited Company?

How to Start a Business in the UK

How to start a business in the UK – Your handy free expert guide on how to start a business in the UK

How to Protect Your Business with Contracts and Agreements

Learn how to protect your business with contracts and agreements. A practical guide for startups

Taking the Leap: The Ultimate Guide to Hiring Your First Employee

Thinking of hiring your first employee? Take a look at our handy guide to understand when and how to recruit.

10 Proven Low-Cost Marketing Strategies for Startups

10 proven low costs marketing strategies which you can implement today to grow your business.

How Much Does It Really Cost to Start a Small Business

Wondering how much it costs to start a small business in the UK? Discover the real start up expenses for entrepreneurs,

Top 20 Home Based Business Ideas

Looking for the best home based business ideas? Discover 20 profitable ways to start a business from home

The Pros and Cons of Running a Business from Home

The Pros and Cons of running a business from home. Considering running a business from home? Read more here.

The Importance of a Business Plan

See why every start-up needs a business plan, what to include in your business plan and why. Easily draft your business plan with our free guidance.

How to Register a Business Name with Companies House: A Step-by-Step Guide for UK Entrepreneurs

Learn how to register a business name with Companies House in the UK. Step-by-step guide covering name rules, fees, documents, etc

Running a Business as a Community Interest Company

Community Interests Company. Get a detailed view of the advantages and disadvantages of running a community interests company

Running a Business as an LLP

Running a business as an LLP. Get an understanding of the LLP business structure with Grow my Acorn

Running a Limited Company in the UK

Considering forming a limited company. Read our guide to see if the Limited Company is the right business structure

Running a Sole Trader Business

Becoming a sole trader. Read our guide to becoming a sole trader and see if it is the right business structure

Running a Business Partnership

Learn how business partnerships work in the UK. Setup, taxes, liability, agreements, pros & cons

Choosing the Right Business Structure

Discover UK business structures: sole trader, partnership, LLP, Ltd, PLC, CIC & charity. Pros & cons explained