What Is Equity Dilution for Founders

What Is Equity Dilution for Founders – Ever heard the term equity dilution? It’s a phrase that can sound a bit intimidating, but the concept is pretty straightforward. In short, it’s what happens to your ownership percentage when your company issues new shares.

For a founder, this is a critical idea to get your head around. Even if the number of shares you personally hold never changes, your slice of the company pie gets smaller every time new investors or employees get their own piece.

The Pizza Analogy: A Simple Way to Understand Dilution

Imagine your new business is a freshly baked pizza. When you start, you own the entire thing—all eight slices. That’s 100% ownership. Simple.

But to grow, you need cash for things like marketing or new equipment. An investor comes along and agrees to give you the money you need, but in return, they want a piece of the action. Instead of handing over some of your own slices, you decide to make the pizza bigger. You add two brand-new slices and give them to the investor.

The pizza now has ten slices in total. You still have your original eight, but here’s the crucial bit: your ownership has changed. Your eight slices no longer represent 100% of the pizza; they now make up 80% (8 out of 10). That drop from 100% to 80%? That’s equity dilution in a nutshell.

Grasping the Core Trade-Off

At first, owning a smaller percentage feels like a loss. But think about what that investor’s cash can do. It could help you buy a better oven, source premium ingredients, and run ads that turn your local pizza joint into a regional chain. The whole pizza becomes much, much more valuable.

The big idea behind accepting dilution is this trade-off: it’s far better to own a smaller percentage of a huge, valuable company than to own 100% of a small one with no room to grow.

This principle is at the heart of what equity dilution means for a startup. It’s not a setback; it’s a strategic move to fuel growth and increase the value of the shares you do have.

Key Terms You Need to Know

To get comfortable with these conversations, there are two terms you’ll hear all the time:

- Shares Outstanding: This is simply the total number of shares a company has issued. In our pizza story, this started at eight slices and grew to ten after the investment.

- Ownership Percentage: This is your slice of the pie. You calculate it by dividing the number of shares you own by the total shares outstanding.

This isn’t just a startup phenomenon; it happens in big public markets too. In the UK, for example, domestic ownership of UK-listed companies fell from 96% in 1981 to just 42% by 2022. This was partly driven by companies issuing new shares and bringing in foreign investors. You can find more insights on UK equity trends from the London Stock Exchange Group.

Ultimately, while your percentage stake goes down, the goal is for the value of your remaining shares to shoot up, making your smaller slice worth far more than your original whole pizza ever could have been.

Why Dilution Is a Necessary Part of Startup Growth

While our pizza analogy makes dilution easy to grasp, it begs an obvious question: why would any founder willingly give up a slice of their company? The answer is simple. Growth needs fuel, and for a young business, that fuel usually comes in the form of capital and talent it doesn’t yet have.

Giving up equity is rarely about losing something. It’s about making a strategic trade—swapping a percentage of ownership for the resources needed to build something far bigger and more valuable. Founders choose this path because it unlocks opportunities that would otherwise be completely out of reach. It’s a fundamental part of the journey when you start to learn how to scale a business effectively.

Securing Capital Through Funding Rounds

The most common reason for dilution is simply raising money. A brilliant idea can only take you so far. To turn that idea into a real, market-ready product, you need cash for development, marketing, operations, and hiring the right people.

This capital is usually raised in stages, known as funding rounds (like Seed, Series A, Series B), and each round brings in new investors who receive newly created shares.

- Practical Example: A Seed Round. A fintech startup wants to build an app but needs £150,000 for development and regulatory approvals. A founder with 100% ownership finds an angel investor. They agree on a £600,000 pre-money valuation. The company issues new shares to the investor for their £150,000, giving them a 20% stake (£150k is 20% of the new £750k post-money valuation). The founder is diluted to 80% but now has the capital to build the product.

This dynamic is happening all over the UK. In 2021 alone, UK small businesses attracted a staggering £18.1 billion in equity investment across 2,616 deals. This flood of capital, from both local and overseas investors, shows just how essential outside funding is for growth—even if it means founders have to dilute their stake. You can dig into more data on these trends from the British Business Bank.

Attracting Top Talent with Share Options

In a competitive market, early-stage startups often can’t go head-to-head with the salaries offered by big, established companies. So, what’s their secret weapon? Equity. By setting up an Employee Share Option Pool (ESOP), founders can offer talented people the chance to own a piece of the company they’re helping to build.

An ESOP is simply a slice of company equity set aside for future hires. When these options are granted and later exercised, they turn into real shares. This, of course, dilutes the ownership of all existing shareholders, including the founders themselves.

Dilution from an ESOP isn’t a loss; it’s a strategic investment in people. Offering equity aligns an employee’s goals with the company’s long-term success, turning them from just an employee into a committed co-owner.

- Practical Example: An ESOP in Action. A founder wants to hire a star software developer who has offers from much larger tech firms. The startup can’t match their salary offers, but it can offer share options from a newly created 10% ESOP. The potential for a huge financial upside convinces the developer to join, bringing skills that accelerate product development and make the whole company more valuable. For the founder, creating this 10% pool means their 80% stake is diluted to 72% (90% of 80%), but they’ve secured a critical team member.

Gaining Speed with Convertible Instruments

Sometimes, a startup needs cash fast, without going through the long, complex process of a priced funding round. This is where convertible instruments come in. Things like SAFEs (Simple Agreements for Future Equity) or convertible notes allow an investor to provide capital now in exchange for the right to get equity later.

This approach lets founders close funding rounds much more quickly, but it creates dilution down the road. When the next official funding round happens, the money from the convertible instrument converts into shares—usually at a discount—which dilutes the existing shareholders even more.

- Practical Example: A Convertible Note. A startup is running low on cash but is close to landing a huge contract. They need £50,000 to tide them over for three months. They sign a convertible note with an investor for £50,000. Six months later, they raise a proper Series A funding round. The £50,000 from the note converts into shares at that new valuation, but with a 20% discount as a reward for the early risk. This causes slightly more dilution than if the investor had participated in the round directly, but the immediate cash injection was vital for survival.

How to Calculate Equity Dilution with Real Examples

Theory is one thing, but seeing the numbers in action makes it all click. To really get your head around what is equity dilution, we need to roll up our sleeves and walk through the calculations step-by-step. Let’s follow the journey of a fictional startup, ‘InnovateUK Ltd.’, to see exactly how a founder’s stake changes over time.

We’ll track our solo founder, Sarah, right from the beginning, through a crucial Seed round and then a Series A round. This will show you not just how dilution happens, but more importantly, how the value of her remaining slice of the pie can grow massively.

Stage 1: The Founder’s Starting Position

Meet Sarah, the founder of InnovateUK Ltd. On day one, she’s the only one in the picture. She issues herself 1,000,000 shares, meaning she owns 100% of the company.

The initial capitalisation table (or ‘cap table’) is as simple as it gets:

| Shareholder | Shares | Ownership |

|---|---|---|

| Sarah (Founder) | 1,000,000 | 100% |

| Total | 1,000,000 | 100% |

At this point, there’s no outside money and no other shareholders. Sarah has total control. But to get her idea off the ground and hire a team, she needs capital.

Stage 2: The Seed Funding Round

InnovateUK Ltd. needs £250,000 to build its first product. Sarah finds an angel investor who’s keen to back her vision. After some negotiation, they settle on a £1,000,000 pre-money valuation – that’s the company’s value before the new cash comes in.

Here’s how the maths breaks down:

- Find the post-money valuation: This is simply the pre-money value plus the new investment.

- £1,000,000 (Pre-Money) + £250,000 (Investment) = £1,250,000 (Post-Money Valuation)

- Work out the investor’s ownership: Divide the investment by the post-money valuation.

- £250,000 / £1,250,000 = 20%

- Calculate the share price: Take the pre-money valuation and divide it by the existing shares.

- £1,000,000 / 1,000,000 shares = £1.00 per share

- Figure out how many new shares to issue: Divide the investment amount by the new share price.

- £250,000 / £1.00 per share = 250,000 new shares

Suddenly, the cap table looks a lot different. The total share count has grown to 1,250,000.

| Shareholder | Shares | Ownership | Value of Stake |

|---|---|---|---|

| Sarah (Founder) | 1,000,000 | 80% | £1,000,000 |

| Angel Investor | 250,000 | 20% | £250,000 |

| Total | 1,250,000 | 100% | £1,250,000 |

You can see Sarah’s ownership has been diluted from 100% down to 80%. But look at the value of her stake – it’s now worth £1,000,000 on paper. This is the classic “smaller slice of a much bigger pie” scenario in action.

Stage 3: The Series A Funding Round

Fast forward a year, and InnovateUK Ltd. is flying. The product is out, customers are signing up, and it’s time to scale. Sarah needs a much bigger investment – £2,000,000 – to pour into sales and marketing.

A venture capital (VC) firm steps in to lead a Series A round, agreeing to an £8,000,000 pre-money valuation. The company’s value has shot up, proving the seed funding did its job.

Let’s run the numbers one more time:

- Calculate the new post-money valuation:

- £8,000,000 (Pre-Money) + £2,000,000 (Investment) = £10,000,000 (Post-Money Valuation)

- Determine the VC’s ownership stake:

- £2,000,000 / £10,000,000 = 20%

- Find the new Series A share price: We use the new pre-money valuation and the total shares outstanding before this round.

- £8,000,000 / 1,250,000 shares = £6.40 per share

- Calculate new shares for the VC firm:

- £2,000,000 / £6.40 per share = 312,500 new shares

The total number of shares has now jumped to 1,562,500 (that’s the old 1,250,000 plus the new 312,500).

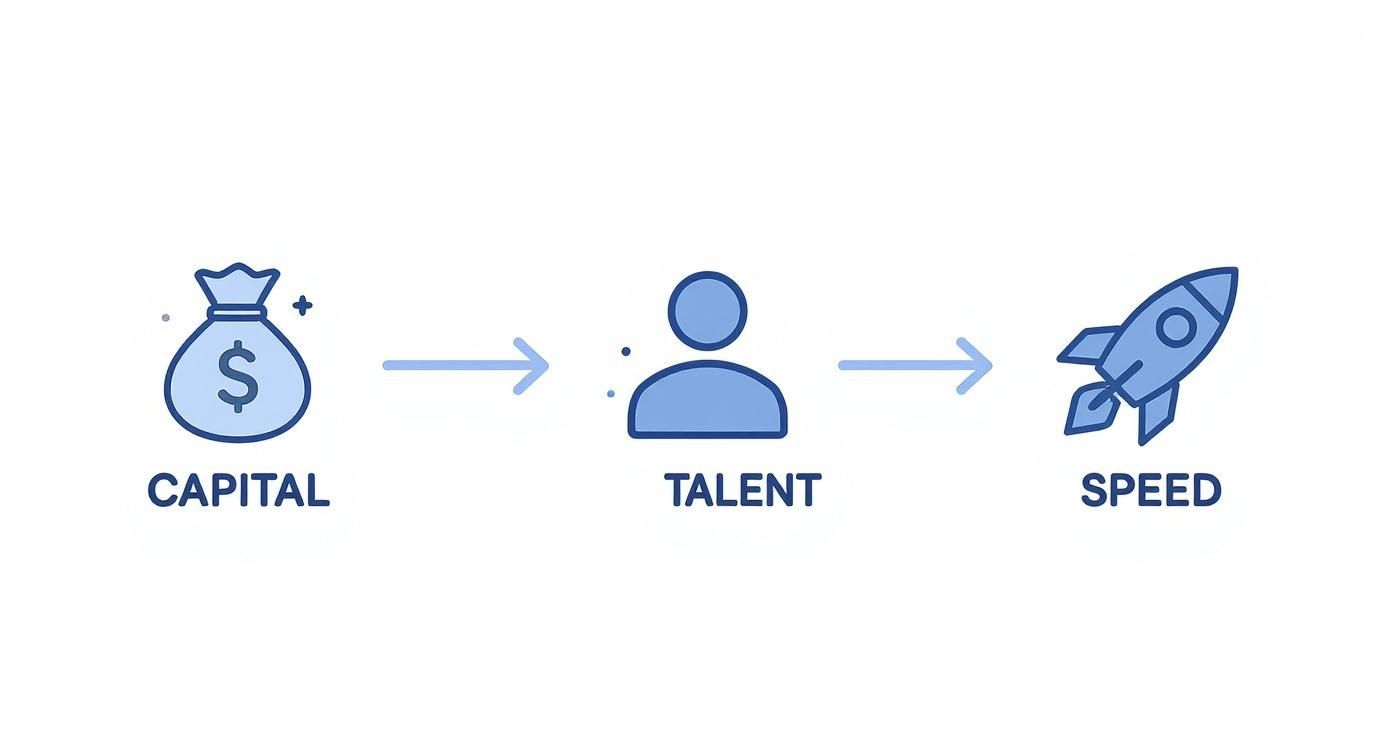

This handy visual shows how strategic dilution fuels growth by injecting capital, attracting talent, and speeding up development.

As the infographic makes clear, dilution isn’t just a financial transaction; it’s a strategic move to build a more valuable and competitive company.

To see the full picture, let’s track how Sarah’s stake has evolved across both funding rounds.

InnovateUK Ltd Cap Table Evolution: Seed vs Series A

The table below breaks down the impact on Sarah’s ownership at each stage. It shows her share count remaining the same, but her percentage ownership decreasing as new shares are created for investors.

| Shareholder | Shares (Pre-Seed) | % Ownership (Pre-Seed) | Shares (Post-Seed) | % Ownership (Post-Seed) | Shares (Post-Series A) | % Ownership (Post-Series A) |

|---|---|---|---|---|---|---|

| Sarah (Founder) | 1,000,000 | 100% | 1,000,000 | 80% | 1,000,000 | 64% |

| Angel Investor | 0 | 0% | 250,000 | 20% | 250,000 | 16% |

| VC Firm | 0 | 0% | 0 | 0% | 312,500 | 20% |

| Total Shares | 1,000,000 | 100% | 1,250,000 | 100% | 1,562,500 | 100% |

After the Series A round, Sarah’s ownership is down to 64%. The angel investor who came in at the seed stage has also been diluted, dropping from 20% to 16%.

So, was it worth it? Let’s look at the value.

The Power of Smart Dilution: Sarah’s ownership dropped from 100% to 80%, and now to 64%. But the paper value of her stake skyrocketed from zero to £1,000,000, and now to an incredible £6,400,000 (64% of the £10m valuation).

This journey perfectly illustrates why founders embrace dilution. Each funding round shrinks your percentage, but if the capital is used well to grow the company’s valuation, the financial outcome for everyone involved gets much, much bigger. With these calculations in your toolkit, you can better understand your own cap table and make informed decisions for your company’s future.

The Human Impact of Dilution on Your Team

While cap tables and spreadsheets show you the maths, they don’t capture the full story. Equity dilution is far more than just numbers on a page; it’s a deeply human process that affects the psychology, motivation, and relationships of everyone pouring their heart and soul into building a company.

To really understand what is equity dilution, you need to appreciate its impact on the very people turning your vision into reality. Each stakeholder experiences this journey differently, navigating a complex trade-off between their personal ownership and the company’s collective growth.

The Founder’s Shifting Role

For a founder, the first few rounds of dilution can be a profound psychological adjustment. It marks the transition from being the sole owner of an idea to becoming the steward of a business with multiple stakeholders who now have a say.

Losing majority control is often the biggest milestone. Suddenly, decisions that were once yours alone now require board approval and investor consensus. This isn’t a failure—it’s a clear sign of success and growth—but it demands a huge change in mindset. You shift from visionary to collaborator.

The weight of responsibility grows, but direct control lessens. It’s also at this stage that founders truly learn the importance of choosing the right partners, a topic we explore in our guide on how to find business partners.

The founder’s journey through dilution is a gradual shift from “my company” to “our company.” It tests your ability to trust others with your vision and to lead through influence rather than direct authority.

This shift can be tough, but successful founders learn to embrace it. They recognise that bringing in experienced investors and talented employees with skin in the game makes the entire enterprise stronger and more resilient.

The Employee Perspective on Stock Options

For employees who join a startup for the promise of equity, dilution is a critical factor in their potential financial outcome. An offer of 10,000 stock options might sound fantastic, but its real value is tied to both the company’s future valuation and the effects of dilution.

Employees must understand that their initial grant represents a percentage of the company at that moment. As new funding rounds happen, that percentage will inevitably shrink.

- Valuation Matters More: An employee’s focus should be less on the raw number of options and more on the company’s potential for growth. Owning 0.1% of a company that becomes worth £100 million is far more valuable than owning 1% of a business that stagnates at £1 million.

- Transparency is Key: Founders who openly communicate about funding rounds and explain how dilution impacts the option pool build enormous trust. When employees understand the “smaller slice of a much bigger pie” logic, they stay motivated and aligned with the company’s long-term goals.

This dynamic shows why a healthy growth trajectory, fuelled by investment, ultimately benefits everyone, even as their individual ownership percentages decrease.

The Early Investor’s Long Game

Angel investors and early backers are the first to take a significant risk on a founder’s vision. They go in knowing their initial stake will almost certainly be diluted over subsequent, larger funding rounds. It’s part of the deal.

Their perspective is all about calculated risk. They know their initial 20% seed-stage ownership might shrink to 5% or even less by the time the company is ready for an exit. Their success depends entirely on that 5% being worth exponentially more than their original investment.

This is a long game, and it’s why dilution is an accepted—and necessary—part of the startup lifecycle for them. It’s a sign that the company is succeeding and attracting the serious capital it needs to scale up and win.

Smart Ways to Manage and Minimise Dilution

Equity dilution is simply part of the startup journey. You can’t avoid it, but it’s definitely not something that just happens to you. As a founder, you can—and should—actively manage the process, protect your stake, and make sure every percentage point you give away brings maximum value in return. It’s about being proactive, not reactive.

Think of it as navigating a river. You can’t stop the current, but with the right tools and a clear map, you can steer your boat effectively. These strategies are your toolkit for having smarter, more confident conversations with investors and making dilution work for you, not against you.

Raise Capital in Stages

One of the most powerful ways to manage dilution is to avoid raising more money than you absolutely need at any one time. Early-stage capital is always the most “expensive” because your company’s valuation is at its lowest. Giving up 20% of your company for £250,000 in a Seed round is far more punishing than giving up 5% for that same amount a few years later when your valuation has shot up.

The smartest approach is staged financing, where you raise just enough cash to hit your next major milestone.

- Seed Round: Get enough to build your minimum viable product (MVP) and win over your first handful of customers.

- Series A: Once you have product-market fit, raise what you need to pour fuel on your sales and marketing fire.

By tying your fundraising to specific, achievable goals, you can justify a higher valuation at each round. This means you give up less equity for every pound raised, which is the key to minimising dilution over the long term.

Negotiate Anti-Dilution Provisions

When you’re sat across the table from investors, certain clauses in your term sheet can protect you from getting hammered by dilution, especially in a “down round”—that dreaded scenario where you raise money at a lower valuation than before. These lifesavers are called anti-dilution provisions.

Anti-dilution provisions are basically an insurance policy for early investors. They adjust an investor’s ownership stake to protect its value if the company’s valuation drops in a future funding round.

There are two main flavours, and you need to know the difference:

- Full Ratchet: This is the harshest and most founder-unfriendly version out there. It reprices all of the early investors’ shares to the new, lower price of the down round. For founders and other shareholders, this can be brutally dilutive. Avoid it if you can.

- Weighted Average: This is a much more common and balanced approach. It adjusts the conversion price for early investors using a formula that takes into account both the old and new share prices, plus the number of new shares being issued. It offers protection without being overly punitive.

Always, always push for a weighted-average clause. It’s the industry standard and signals that you know how to protect your own equity while still being fair to your investors. This is a critical detail that needs to be formalised. Using a solid framework like a free shareholder agreement template from the start can make sure these terms are crystal clear.

Be Smart About Your Option Pool Timing

Creating an employee share option pool (ESOP) is non-negotiable for attracting top talent, but when you create or expand it matters immensely. Investors will almost always insist that the ESOP is created or topped up as part of their investment, and they’ll want it done using the pre-money valuation.

This is a crucial detail. If the option pool comes out of the pre-money share total, only the existing shareholders (that’s you, the founder) get diluted. If it’s created post-money, the new investors are diluted right along with everyone else.

Here’s a practical example: An investor agrees to a £4 million pre-money valuation and wants a 10% option pool set up for new hires. If this is done “pre-money”, the company creates the 10% pool first, effectively reducing the founder’s ownership before the investment cash comes in. The founder’s stake takes the entire hit of this dilution. You should always negotiate to keep this pre-money option pool as small as is realistic, justifying its size with a clear hiring plan for the next 12-18 months. Don’t create a bigger pool than you need just to keep an investor happy.

Common Questions About Equity Dilution

As founders and early employees get to grips with equity, a few questions seem to pop up time and time again. Understanding the theory of dilution is one thing, but figuring out how it applies in the real world can feel a bit abstract. Here are some clear, straightforward answers to the most common sticking points.

How Does My First Investment Cause Dilution When I Am The Only Owner?

This is a classic and completely logical question. If you own 100% of the company, how can an investor get a piece without you physically giving them some of your shares?

The key is to remember that you’re not handing over your existing shares; the company is creating brand-new ones just for the investor.

Imagine your company has 1,000,000 shares, and you own all of them. To raise money, the company authorises and issues 250,000 new shares and sells them to an investor. You still hold your original 1,000,000 shares, but the total number of shares in existence (the ‘shares outstanding’) has just increased to 1,250,000.

Your ownership is now your shares divided by this new, larger total (1,000,000 / 1,250,000), which means your stake is 80%. The dilution happened because the total size of the pie grew, not because your slice was cut down.

What Is The Difference Between Economic and Voting Dilution?

While they’re often linked, economic and voting dilution are two different things, affecting separate aspects of your role in the business. It’s vital to understand both.

- Economic Dilution: This is all about the money. It’s the reduction in your financial ownership percentage, which directly impacts your share of future profits or the proceeds from a sale. Every time new shares are issued, your economic stake gets a little smaller.

- Voting Dilution: This is about your influence and control. If each share gets one vote, issuing new shares reduces your percentage of the total voting power. This can affect your ability to pass resolutions, appoint directors, or approve big strategic decisions.

It’s possible to have one without the other. For instance, a company could issue non-voting shares to new investors. This would cause economic dilution for existing shareholders but wouldn’t touch their voting control.

How Do Convertible Notes Affect Dilution Compared to a Priced Round?

Convertible notes (and their close cousins, SAFEs) are hugely popular for early-stage funding because they’re faster and simpler than a traditional priced round. But they handle dilution very differently.

A priced round, like a Series A, causes immediate and clear dilution. You and your investors agree on a company valuation, set a share price, and issue a specific number of new shares. The dilution is calculated and locked in the moment the deal closes. Simple.

A convertible note, on the other hand, is essentially a loan that turns into equity at a future funding round. This means it defers the dilution. You get the cash now, but you won’t know the exact dilution impact until that note converts down the line. To reward the early investor for their risk, the note usually converts at a discount to the future share price, which means the eventual dilution is slightly greater for you than it is for the new investors in that later round.

Can I Avoid Dilution Completely if My Business Is Profitable?

Yes, absolutely—but it comes with some serious trade-offs. A business that funds its growth entirely from its own profits is known as a bootstrapped company. By never taking external equity investment, the founders can retain 100% ownership and avoid dilution completely.

However, this path isn’t for everyone. Bootstrapping almost always means slower growth. When you rely solely on profits, you limit your ability to make big, aggressive moves in marketing, hiring, or product development. Meanwhile, your competitors who are taking on investment and diluting their equity could use that capital to scale much faster and capture the market.

Ultimately, the choice comes down to your personal goals. If maintaining total control and ownership is your absolute top priority, bootstrapping is the way to go. But if your ambition is to build a large, market-leading company as quickly as possible, then strategic equity dilution is almost always a necessary part of the journey.

Navigating the complexities of equity, ownership, and business growth can be challenging. At Grow My Acorn, we provide the information, help, and advice that entrepreneurs and company directors need to make informed decisions. Explore our resources to build your business with confidence at https://growmyacorn.co.uk.

More Topics

What is invoice factoring: A Clear Guide to Faster Cash Flow

Discover what is invoice factoring and how it unlocks fast cash flow for your business with simple examples and practical steps.

12 Profitable Self Employment Ideas to Start in 2025

Discover 12 practical self employment ideas you can launch this year. Our guide covers startup costs, skills, and

How to Delegate Effectively: Master Your Team Productivity

Discover how to delegate effectively with practical tips to boost team productivity, empower others, and drive better results.

How to Build an Email List from Scrath

Learn how to build an email list with our practical guide. Discover actionable strategies and expert tips to grow an audience that converts.

How to Improve Employee Retention

Discover how to improve employee retention with actionable strategies on leadership, compensation, and culture

Streamlining business processes: Boost efficiency today

Discover how streamlining business processes can unlock efficiency and drive growth with practical, actionable steps.

marketing tips for small business: 5 quick wins

Uncover marketing tips for small business that boost ROI with 5 practical strategies you can implement this week

what is professional indemnity insurance? A quick guide

what is professional indemnity insurance: learn what it covers, who needs it, and how to choose the right PI policy for your business.

10 Actionable Marketing Tips for Small Businesses in 2025

Discover 10 practical marketing tips for small businesses. Boost your growth with budget-friendly strategies for SEO,

10 Profitable Business Ideas UK from Home for 2025

Discover 10 practical profitable business ideas UK from home. This guide covers startup costs, income potential,

What Is a Break Even Analysis Explained

What is a break even analysis? Learn how to calculate it and use this simple tool to make smarter financial decisions for your business.

How to Create a Cash Flow Forecast That Works

Learn how to create a cash flow forecast with this practical guide. We cover predicting inflows, mapping outflows,

How to Write a Business Proposal That Wins Clients

Learn how to write a business proposal that actually wins clients. Offering advice and real-world examples

How to Conduct Competitor Analysis That Drives Growth

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

How to Register a Business in the UK Your Complete Guide

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

12 Best Ways to Advertise Your Business in 2025

12 Best Ways to Advertise Your Business Discover the best ways to advertise your business

Small Business Accounting Basics Made Simple

Master small business accounting basics with our guide. Learn bookkeeping, financial statements, and tax

Business Exit Strategy Planning Done Right

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Find Business Partners That Actually Fit

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

High Street vs Digital Business Banking

Compare High Street vs Digital Business Banking for start-ups. Discover the pros and cons of business banking

10 Crucial Pieces of Business Advice for Startups

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

How to Scale a Business The Right Way

Learn how to scale a business with proven, real-world strategies. The complete guide

A Board Meeting Agenda Template That Actually Works

Tired of unproductive meetings? Use our board meeting agenda template to drive focus, ensure compliance

Sole Trader Tax Deductions

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Build Business Credit for Your UK Business

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

What Is a Business Model Canvas?

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Improve Customer Service A UK Business Guide

Discover how to improve customer service with actionable strategies for UK businesses

Dealing with Difficult Clients: Top Strategies for Success

Dealing with difficult clients isn’t about winning arguments. Learn how to deal with difficult clients.

Business Plan Executive Summary Examples: 8 Inspiring Samples

How to professionally prepare your business plan executive summary along with practical examples.

Your Guide to a Business Risk Management Framework

Build a robust business risk management framework with our free online guidance.

How to Improve Cash Flow: Proven Tips for UK Businesses

Learn how to improve cash flow with actionable strategies for UK businesses. Master invoicing, managing expenses

Social Media Marketing for Small Business

Social Media Marketing for Small Business Free Expert Guidance from Grow My Acorn the ultimate free resource

10 Powerful Customer Retention Strategies for 2025

Discover 10 actionable customer retention strategies with real examples. Learn how to boost loyalty,

How to Grow a Business The Right Way

How to Grow a Business The Right Way grow your business the right way with free expert advice

Proven Marketing Strategies for Small Businesses

Get your marketing strategy off to a flying start with our proven strategies guaranteed to deliver measurable results.

Sole Trader vs Limited Company UK Guide

Choose the right business structure. Understand the differences, benefits and pitfalls. Sole Trader? Limited Company?

How to Start a Business in the UK

How to start a business in the UK – Your handy free expert guide on how to start a business in the UK

How to Protect Your Business with Contracts and Agreements

Learn how to protect your business with contracts and agreements. A practical guide for startups

Taking the Leap: The Ultimate Guide to Hiring Your First Employee

Thinking of hiring your first employee? Take a look at our handy guide to understand when and how to recruit.

10 Proven Low-Cost Marketing Strategies for Startups

10 proven low costs marketing strategies which you can implement today to grow your business.

How Much Does It Really Cost to Start a Small Business

Wondering how much it costs to start a small business in the UK? Discover the real start up expenses for entrepreneurs,

Top 20 Home Based Business Ideas

Looking for the best home based business ideas? Discover 20 profitable ways to start a business from home

The Pros and Cons of Running a Business from Home

The Pros and Cons of running a business from home. Considering running a business from home? Read more here.

The Importance of a Business Plan

See why every start-up needs a business plan, what to include in your business plan and why. Easily draft your business plan with our free guidance.

How to Register a Business Name with Companies House: A Step-by-Step Guide for UK Entrepreneurs

Learn how to register a business name with Companies House in the UK. Step-by-step guide covering name rules, fees, documents, etc

Running a Business as a Community Interest Company

Community Interests Company. Get a detailed view of the advantages and disadvantages of running a community interests company

Running a Business as an LLP

Running a business as an LLP. Get an understanding of the LLP business structure with Grow my Acorn

Running a Limited Company in the UK

Considering forming a limited company. Read our guide to see if the Limited Company is the right business structure

Running a Sole Trader Business

Becoming a sole trader. Read our guide to becoming a sole trader and see if it is the right business structure

Running a Business Partnership

Learn how business partnerships work in the UK. Setup, taxes, liability, agreements, pros & cons

Choosing the Right Business Structure

Discover UK business structures: sole trader, partnership, LLP, Ltd, PLC, CIC & charity. Pros & cons explained