What is Invoice Factoring

What is Invoice Factoring – Picture this: you’ve just completed a big job, sent the invoice, and now… you wait. Thirty, sixty, maybe even ninety days for the cash to actually hit your account. This waiting game is a huge source of frustration for businesses, tying up money you’ve already earned.

What if you could get paid almost instantly? That’s the simple, powerful idea behind invoice factoring.

What Is Invoice Factoring and How Can It Help My Business?

At its core, invoice factoring isn’t a loan. Think of it more like cashing in your invoices early. You sell your unpaid invoices to a third-party company (known as a ‘factor’) at a slight discount. In return, they give you the bulk of the money straight away.

Instead of your team chasing payments or juggling a slow-moving sales ledger, you turn those outstanding invoices into immediate, usable cash. This completely changes your cash flow dynamic.

For example, a haulage company might complete a £5,000 delivery but have to wait 60 days for payment. With factoring, they could receive around £4,250 of that cash within 24 hours, allowing them to pay for fuel and driver wages immediately instead of waiting for the client to pay.

Within 24 to 48 hours, you can receive up to 90% of an invoice’s value. That’s working capital you can use right now to cover payroll, buy stock, or jump on a new growth opportunity without a moment’s hesitation.

A Stronger Foundation for Your Business

For small and medium-sized businesses (SMEs) in particular, this kind of financial stability is a game-changer. It’s no surprise that invoice factoring has become such a popular tool for navigating cash flow hurdles here in the UK.

By unlocking the money tied up in your sales ledger, you can fund growth and meet day-to-day expenses without taking on new debt. Your accounts receivable ledger transforms from a list of promises into a genuine, powerful asset.

And it’s not a niche solution, either. As of 2024, over 55,000 UK businesses were using invoice factoring, a clear sign of just how practical and widely adopted it has become. If you’d like to dig deeper into its role in the UK economy, you can discover more insights about invoice factoring in the UK.

A Practical Walkthrough of the Factoring Process

Theory is one thing, but to really get your head around invoice factoring, you need to see it in action. Let’s walk through a real-world scenario to see exactly how the cash from an unpaid invoice can flow straight into your business bank account.

Imagine a small creative agency, “BrightSpark Designs,” has just finished a big branding project for a corporate client. They send out an invoice for £10,000 with their standard 60-day payment terms. The money is technically theirs, but waiting two months creates a cash flow squeeze, making it tough to pay their freelance designers and invest in new software.

From Invoice to Immediate Capital

Instead of waiting, BrightSpark decides to work with a factoring company. This is where the magic happens, turning a future payment into cash they can use today. The whole process is designed to be quick and surprisingly simple, often taking just a couple of days from start to finish.

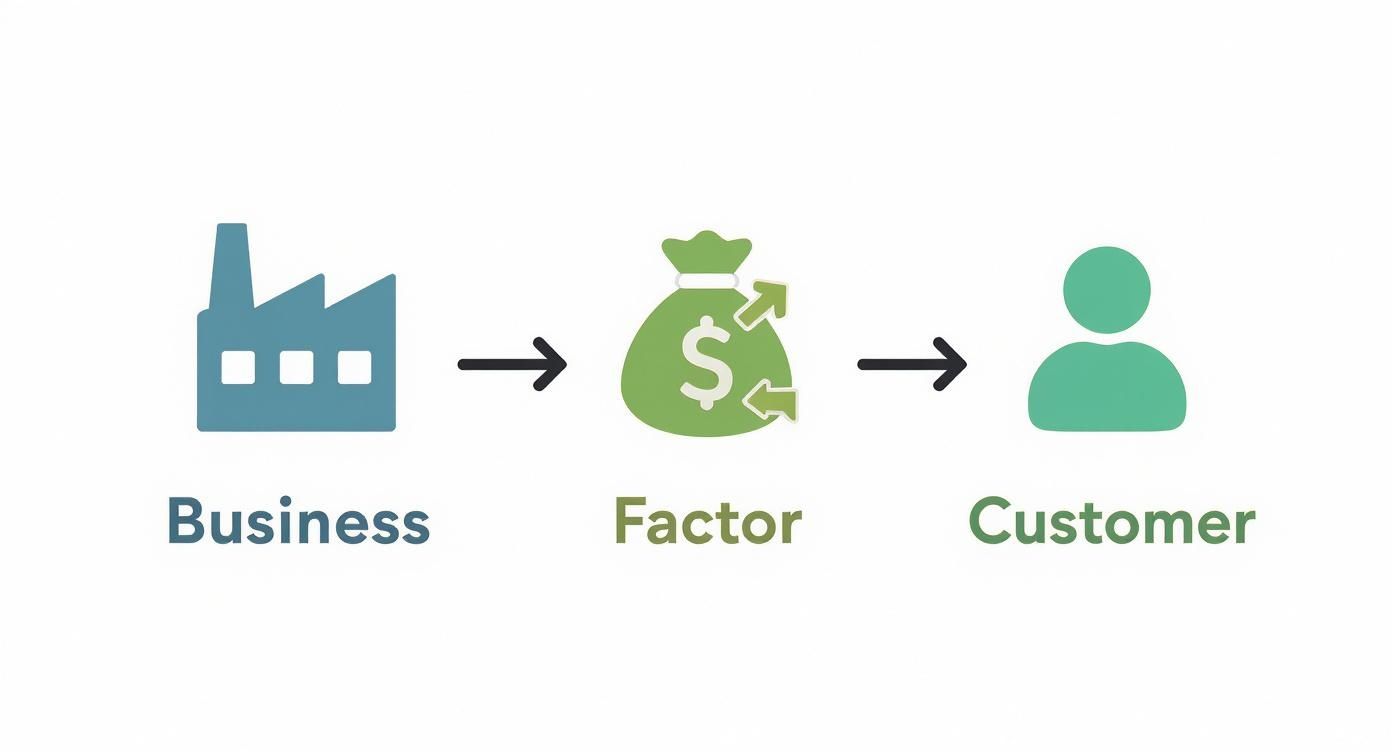

This visual breaks down the flow between the business (you), the factor, and your customer.

As you can see, the factor essentially acts as a financial middleman, unlocking cash for your business long before the customer’s payment due date even arrives.

The Five Key Steps

The whole thing unfolds in a clear, organised sequence. Here’s exactly how BrightSpark gets its cash:

- Invoice Submission: The agency uploads its £10,000 invoice to the factoring company’s online portal for a quick verification.

- Initial Advance: Within 24 to 48 hours, the factor approves the invoice and advances 85% of its value—that’s £8,500—straight into BrightSpark’s bank account. Their immediate cash flow problem is solved.

- Professional Collections: The factoring company’s credit control team now takes over chasing the payment. They’ll contact BrightSpark’s client politely and professionally when the invoice is due, preserving the customer relationship.

- Customer Payment: On day 60, the client pays the full £10,000 invoice directly to the factoring company, just as instructed.

- Final Settlement: The factor then pays the remaining 15% (£1,500) to BrightSpark, minus their small, pre-agreed fee for the service.

This step-by-step process shows how factoring provides an immediate and practical cash flow benefit. It’s not a loan; it’s simply a way to get your hands on the money you’ve already earned, but faster.

This straightforward approach helps businesses stay financially healthy without disrupting their day-to-day operations. Effectively managing this flow of money is a cornerstone of good financial management, and for anyone wanting to brush up on the fundamentals, understanding small business accounting basics is a great place to start.

By turning receivables into ready cash, companies like BrightSpark can stop chasing payments and get back to focusing on growth.

Understanding Your Factoring Options

Invoice factoring isn’t a one-size-fits-all solution. Think of it more like a toolkit – the right tool depends entirely on the job you need to do. Different arrangements suit different business needs, risk appetites, and cash flow patterns, so understanding your options is key to making the right choice.

The first, and arguably most important, decision you’ll face is between recourse and non-recourse factoring. This choice boils down to one simple question: who carries the risk if your customer doesn’t pay?

Recourse vs Non-Recourse Factoring

Recourse factoring is the most common and affordable route. With this setup, you sell your invoices to the factor, but you ultimately remain on the hook if your customer fails to pay. If the invoice goes unpaid after an agreed period (usually 90 days), you’ll either have to buy it back or replace it with another invoice of a similar value.

- Practical Example: A small printing company uses recourse factoring for a £2,000 invoice. Their client unexpectedly goes out of business and doesn’t pay. After 90 days, the printing company must repay the initial cash advance to the factoring provider.

Because the factoring company’s risk is much lower, they pass those savings on to you in the form of smaller fees. It’s a great option if you have a reliable client base and want to keep costs down.

Non-recourse factoring, on the other hand, is like buying an insurance policy for your invoices. The factoring company assumes most of the risk of your customer not paying due to declared insolvency. If your client goes bankrupt and can’t settle their bill, the factor takes the financial hit, not you.

- Practical Example: A recruitment agency places a candidate and invoices £8,000 on 60-day terms. They use non-recourse factoring. On day 45, their client declares bankruptcy. The recruitment agency gets to keep the advance they received, and the factoring company absorbs the loss.

This extra protection comes at a price – non-recourse agreements have higher fees to cover the additional risk the factor is taking on.

It’s crucial to understand the fine print here. Non-recourse protection typically only covers client insolvency. It won’t cover commercial disputes where a client refuses to pay because they’re unhappy with the goods or services you provided.

Spot Factoring vs Whole-Ledger Factoring

The next big decision is how many of your invoices you want to factor. Are you looking for a quick, one-off cash boost, or do you need a continuous, reliable source of funding?

- Spot Factoring: This is perfect for businesses that need a fast, targeted cash injection. It lets you pick a single invoice (or a small handful) to sell without committing to a long-term contract. It’s the ideal tool for covering an unexpected bill or seizing a sudden growth opportunity that you’d otherwise miss. A classic example is a construction firm factoring a single large invoice for a completed project phase to buy materials for the next one.

- Whole-Ledger Factoring: Often called a factoring facility, this is an ongoing arrangement where you agree to factor all, or a large portion, of your sales ledger. This approach provides a consistent and predictable stream of working capital, turning your unpaid invoices into a reliable flow of cash to run your day-to-day operations. For instance, a wholesale food supplier might use this to maintain a steady cash flow for purchasing stock, despite their supermarket clients paying on 90-day terms.

This kind of flexibility has made factoring a hugely popular financial tool across Europe, with the United Kingdom being a major player. The market has seen incredible growth, with total factoring volume jumping from EUR 1,844,721 million in 2020 to EUR 2,555,266 million in 2023. You can discover more insights about European factoring statistics on market.us.

Calculating the True Cost of Invoice Factoring

To really get a grip on what invoice factoring will cost, you need to look past the headline rates and break down the fees. The good news is that the fee structure is usually quite straightforward, designed to be transparent so you can accurately see how it impacts your bottom line. Without that clarity, trying to compare offers from different providers is just guesswork.

You’ll almost always come across two main charges: the discount fee and the service fee. The easiest way to think of them is as the cost of borrowing and the cost of administration.

The Two Main Factoring Fees

- Discount Fee (or Factoring Fee): This is the main cost. It’s a percentage of your invoice’s total value, typically ranging from 1% to 4%. This rate often changes depending on how long your customer takes to pay—the faster they settle up, the lower your fee.

- Service Fee (or Admin Fee): This covers all the behind-the-scenes work the factoring company does for you, like managing your sales ledger, running credit control, and chasing up late payments. It might be a fixed monthly fee or a small percentage of your annual turnover.

A Practical Cost Example

Let’s walk through a real-world example to see how this plays out. Imagine your business has a £20,000 invoice you want to factor. The provider offers an 85% advance rate with a 2% discount fee.

Here’s the step-by-step breakdown:

- Initial Advance: The factor immediately pays you £17,000 upfront (which is 85% of £20,000).

- Customer Pays: Your customer pays the full £20,000 directly to the factoring company when the invoice is due.

- Fees Are Deducted: The factor calculates their fee: 2% of the £20,000 invoice total comes to £400.

- Final Payment: You receive the leftover amount. That’s the £3,000 reserve (the final 15%) minus their £400 fee, leaving you with a final payment of £2,600.

In this scenario, the total cost to get your hands on £17,000 almost instantly was £400. You can plug these kinds of figures into a free cashflow forecast template to visualise exactly how an immediate cash injection could transform your operations.

This kind of pricing is pretty typical. In the UK, the average cost for factoring services works out to be around 1.27% of a business’s annual turnover, showing just how common and competitive this funding route has become.

Is Invoice Factoring the Right Move for Your Business?

Deciding on the right funding path means taking an honest look at where your business is today and where you want it to go. Invoice factoring is a powerful tool, no doubt, but whether it’s the right tool depends entirely on your specific circumstances, goals, and even your industry.

For many businesses, the main driver is simple: immediate cash flow relief. If you’re constantly stuck in the gap between sending an invoice and actually getting paid, factoring is designed to solve that exact problem. It bridges that cash gap, making sure you have the working capital you need for payroll, new stock, or just covering day-to-day costs without the stress.

But the benefits go beyond just getting your hands on cash faster. When you hand over your collections to the factoring company, you’re also buying back your team’s most valuable resource: time. Instead of chasing late payments, your staff can focus on the things that actually grow the business, like sales, customer service, and product development.

Who Benefits Most From Factoring?

While lots of businesses can use factoring, some are a near-perfect fit. If your business falls into one of these categories, it’s a strong sign that factoring could be a game-changer for you.

- High-Growth B2B Companies: Businesses that are scaling up fast often find their growth outpaces their cash flow. Factoring gives you the immediate capital to say “yes” to bigger orders and new contracts without hesitation.

- Businesses with Long Payment Terms: If you work in an industry like manufacturing, recruitment, or logistics, you’ll be all too familiar with 60 or 90-day payment cycles. Factoring transforms those long waits into a predictable, steady stream of cash.

- Startups Needing Working Capital: New businesses often don’t have the trading history or assets needed for a traditional bank loan. Factoring companies care more about the creditworthiness of your customers, making it a much more accessible way to get funded.

The real beauty of factoring is that it lets you fund growth without taking on debt. You’re not borrowing money; you’re just accessing the cash you’ve already earned, only much, much faster.

Weighing the Potential Downsides

Of course, no financial solution is perfect. The most obvious trade-off is the cost. Factoring is typically more expensive than a traditional business loan. You’re paying a premium for speed, flexibility, and the admin support that comes with it, so you need to be sure that having immediate access to your cash is worth the fee.

The other thing to consider is the customer relationship. A professional factoring company will always treat your clients with respect, but you are introducing a third party into your payment process. For some business owners, this can feel like losing a bit of control over a critical part of their customer interactions.

Ultimately, the decision comes down to a simple calculation. If the need for reliable cash flow and outsourced credit control outweighs the costs and the third-party involvement, then invoice factoring is very likely the right move for your business.

How Factoring Compares to Other Finance Options

Invoice factoring is a powerful tool for unlocking cash, but it’s just one of several ways to fund your business. Understanding where it fits alongside other options is the key to making the right choice. The best path forward really depends on what your business needs most: immediate cash, long-term control, or the lowest possible cost.

Each option works very differently. Factoring pulls cash forward from your sales ledger, a business loan injects fresh capital but creates debt, and invoice discounting offers a quieter way to borrow against your invoices. Seeing them side-by-side will make it much clearer which one fits your goals.

Factoring vs Traditional Business Loans

The biggest difference between factoring and a traditional bank loan comes down to what the lender is looking at. A bank loan is all about your business’s creditworthiness. Lenders will want to see your trading history, credit score, and what assets you have before they’ll even consider an application. This process can be painstakingly slow, often dragging on for weeks or even months.

Invoice factoring, on the other hand, flips this on its head. It focuses on the creditworthiness of your customers. The factoring company is far more interested in whether your clients are reliable and have a solid history of paying on time. This makes it a fantastic option for new or fast-growing businesses that simply don’t have the long track record a bank would demand.

Another crucial point is debt.

- Business Loan: You get a lump sum of cash that you have to pay back, with interest, over a fixed period. This adds a new liability to your balance sheet.

- Invoice Factoring: You’re essentially selling an asset—your unpaid invoices—to get money you’ve already earned. It’s not a loan, so you’re not taking on any new debt.

Factoring vs Invoice Discounting

Invoice discounting is often seen as factoring’s close cousin, but there’s a critical difference: who deals with your customers. Both let you borrow against your unpaid invoices, but they part ways when it comes to chasing payments and how confidential the arrangement is.

With invoice factoring, the provider takes over your credit control. They manage your sales ledger and chase your customers for payment directly. This is a huge plus if you want to outsource a time-consuming admin task and free up your team.

Invoice discounting, however, is a more discreet service. You still get the funding, but you keep full control over your sales ledger and customer communications. Your clients usually have no idea a third party is involved. This option is typically a better fit for larger, more established businesses that already have a dedicated credit control team in-house.

You can learn more about managing your finances and how to improve cash flow in our detailed guide.

Common Questions About Invoice Factoring

Even after weighing up the pros and cons, most business owners still have a few practical questions floating around. Let’s tackle some of the most common ones we hear from entrepreneurs, especially those running new or small businesses.

Can a New Business Use Invoice Factoring?

Yes, absolutely. This is probably one of the biggest myths about business finance—that you need a long track record to get funding.

Unlike a traditional bank loan where they pore over your company’s history, factoring companies are more interested in the financial strength of your customers. As long as you’re invoicing reputable, creditworthy businesses, your chances of approval are high, even if you only started trading last month. It’s a great way for startups to get off the ground.

Will My Customers Know I Am Using a Factoring Service?

In most cases, yes. With standard invoice factoring, the finance provider takes over the credit control process. This means they’ll be the ones chasing the payment, so your customer will know you’re working with a third party.

But don’t worry, this isn’t a bad thing. Professional factoring companies are experts in customer relations. They know how to be polite and persistent without damaging your hard-won relationships. These days, it’s such a common practice that most businesses just see it as a sign of an organised, professional operation.

Key Takeaway: Many businesses find that using a professional collections service actually improves their payment times. It signals you have solid financial processes in place, which can strengthen your professional image, not weaken it.

Is There a Minimum Invoice Size to Get Started?

This really varies from one provider to another. Some of the old-school factors might prefer chunky invoices or require a minimum annual turnover to set up a full facility.

However, the industry has changed a lot. Many modern providers, especially those offering spot factoring, are incredibly flexible. They specialise in supporting smaller businesses and startups, so they’ve scrapped the strict minimums. It’s always worth asking, even if you feel your invoices are on the small side. For them, it’s about the reliability of the debt, not just the amount.

At Grow My Acorn, our goal is to give you clear, practical advice to help your business thrive. For more guides and resources designed for entrepreneurs and small business owners, visit us at https://growmyacorn.co.uk.

More Topics

12 Profitable Self Employment Ideas to Start in 2025

Discover 12 practical self employment ideas you can launch this year. Our guide covers startup costs, skills, and

How to Delegate Effectively: Master Your Team Productivity

Discover how to delegate effectively with practical tips to boost team productivity, empower others, and drive better results.

How to Build an Email List from Scrath

Learn how to build an email list with our practical guide. Discover actionable strategies and expert tips to grow an audience that converts.

How to Improve Employee Retention

Discover how to improve employee retention with actionable strategies on leadership, compensation, and culture

Streamlining business processes: Boost efficiency today

Discover how streamlining business processes can unlock efficiency and drive growth with practical, actionable steps.

marketing tips for small business: 5 quick wins

Uncover marketing tips for small business that boost ROI with 5 practical strategies you can implement this week

what is professional indemnity insurance? A quick guide

what is professional indemnity insurance: learn what it covers, who needs it, and how to choose the right PI policy for your business.

10 Actionable Marketing Tips for Small Businesses in 2025

Discover 10 practical marketing tips for small businesses. Boost your growth with budget-friendly strategies for SEO,

10 Profitable Business Ideas UK from Home for 2025

Discover 10 practical profitable business ideas UK from home. This guide covers startup costs, income potential,

What Is a Break Even Analysis Explained

What is a break even analysis? Learn how to calculate it and use this simple tool to make smarter financial decisions for your business.

How to Create a Cash Flow Forecast That Works

Learn how to create a cash flow forecast with this practical guide. We cover predicting inflows, mapping outflows,

How to Write a Business Proposal That Wins Clients

Learn how to write a business proposal that actually wins clients. Offering advice and real-world examples

What Is Equity Dilution for Founders

Understand what is equity dilution and how it impacts your startup. Our guide explains cap tables, funding rounds

How to Conduct Competitor Analysis That Drives Growth

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

How to Register a Business in the UK Your Complete Guide

Learn how to register a business in the UK with our practical guide. We cover sole trader and limited company setups

12 Best Ways to Advertise Your Business in 2025

12 Best Ways to Advertise Your Business Discover the best ways to advertise your business

Small Business Accounting Basics Made Simple

Master small business accounting basics with our guide. Learn bookkeeping, financial statements, and tax

Business Exit Strategy Planning Done Right

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Find Business Partners That Actually Fit

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

High Street vs Digital Business Banking

Compare High Street vs Digital Business Banking for start-ups. Discover the pros and cons of business banking

10 Crucial Pieces of Business Advice for Startups

Discover essential business advice for startups to thrive. Complete guide from Grow My Acorn

How to Scale a Business The Right Way

Learn how to scale a business with proven, real-world strategies. The complete guide

A Board Meeting Agenda Template That Actually Works

Tired of unproductive meetings? Use our board meeting agenda template to drive focus, ensure compliance

Sole Trader Tax Deductions

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Build Business Credit for Your UK Business

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

What Is a Business Model Canvas?

Learn what is a business model canvas and how this one-page tool helps startups visualise, test, and refine

How to Improve Customer Service A UK Business Guide

Discover how to improve customer service with actionable strategies for UK businesses

Dealing with Difficult Clients: Top Strategies for Success

Dealing with difficult clients isn’t about winning arguments. Learn how to deal with difficult clients.

Business Plan Executive Summary Examples: 8 Inspiring Samples

How to professionally prepare your business plan executive summary along with practical examples.

Your Guide to a Business Risk Management Framework

Build a robust business risk management framework with our free online guidance.

How to Improve Cash Flow: Proven Tips for UK Businesses

Learn how to improve cash flow with actionable strategies for UK businesses. Master invoicing, managing expenses

Social Media Marketing for Small Business

Social Media Marketing for Small Business Free Expert Guidance from Grow My Acorn the ultimate free resource

10 Powerful Customer Retention Strategies for 2025

Discover 10 actionable customer retention strategies with real examples. Learn how to boost loyalty,

How to Grow a Business The Right Way

How to Grow a Business The Right Way grow your business the right way with free expert advice

Proven Marketing Strategies for Small Businesses

Get your marketing strategy off to a flying start with our proven strategies guaranteed to deliver measurable results.

Sole Trader vs Limited Company UK Guide

Choose the right business structure. Understand the differences, benefits and pitfalls. Sole Trader? Limited Company?

How to Start a Business in the UK

How to start a business in the UK – Your handy free expert guide on how to start a business in the UK

How to Protect Your Business with Contracts and Agreements

Learn how to protect your business with contracts and agreements. A practical guide for startups

Taking the Leap: The Ultimate Guide to Hiring Your First Employee

Thinking of hiring your first employee? Take a look at our handy guide to understand when and how to recruit.

10 Proven Low-Cost Marketing Strategies for Startups

10 proven low costs marketing strategies which you can implement today to grow your business.

How Much Does It Really Cost to Start a Small Business

Wondering how much it costs to start a small business in the UK? Discover the real start up expenses for entrepreneurs,

Top 20 Home Based Business Ideas

Looking for the best home based business ideas? Discover 20 profitable ways to start a business from home

The Pros and Cons of Running a Business from Home

The Pros and Cons of running a business from home. Considering running a business from home? Read more here.

The Importance of a Business Plan

See why every start-up needs a business plan, what to include in your business plan and why. Easily draft your business plan with our free guidance.

How to Register a Business Name with Companies House: A Step-by-Step Guide for UK Entrepreneurs

Learn how to register a business name with Companies House in the UK. Step-by-step guide covering name rules, fees, documents, etc

Running a Business as a Community Interest Company

Community Interests Company. Get a detailed view of the advantages and disadvantages of running a community interests company

Running a Business as an LLP

Running a business as an LLP. Get an understanding of the LLP business structure with Grow my Acorn

Running a Limited Company in the UK

Considering forming a limited company. Read our guide to see if the Limited Company is the right business structure

Running a Sole Trader Business

Becoming a sole trader. Read our guide to becoming a sole trader and see if it is the right business structure

Running a Business Partnership

Learn how business partnerships work in the UK. Setup, taxes, liability, agreements, pros & cons

Choosing the Right Business Structure

Discover UK business structures: sole trader, partnership, LLP, Ltd, PLC, CIC & charity. Pros & cons explained